Using a HELOC to Buy a Second Home: Pros, Cons & Mortgage Insights

For many homeowners in 2026, the greatest financial asset isn’t sitting in a savings account—it’s locked within the walls of their primary residence. As home values have maintained a steady upward trajectory over the last several years, tappable equity has reached record highs. If you are looking to expand your real estate portfolio or secure a vacation getaway, using a HELOC to buy a second home has emerged as a premier strategy for savvy investors and families alike.

Leveraging equity allows you to bypass the hurdles of liquidating cash reserves or selling off stocks in a volatile market. However, navigating the mortgage landscape in 2026 requires a nuanced understanding of interest rate trends and debt-to-income ratios. This guide explores how a Home Equity Line of Credit (HELOC) works and whether it is the right engine to power your next property purchase.

What Is a HELOC and How It Works

Despite regulatory shifts in some cities, the short‑term rental market remains strong. According to AirDNA’s 2025 U.S. Short‑Term Rental Outlook, national STR demand grew 7.8% year‑over‑year, and average daily rates increased 3.2% heading into 2026. Investor interest remains high because:

STRs often generate 20–40% higher gross rental income than comparable long‑term rentals in the same market.

Remote work and flexible travel trends continue to support year‑round occupancy.

Many secondary and tertiary markets have seen rising tourism and fewer regulatory restrictions.

However, higher potential returns also come with more complex financing requirements.

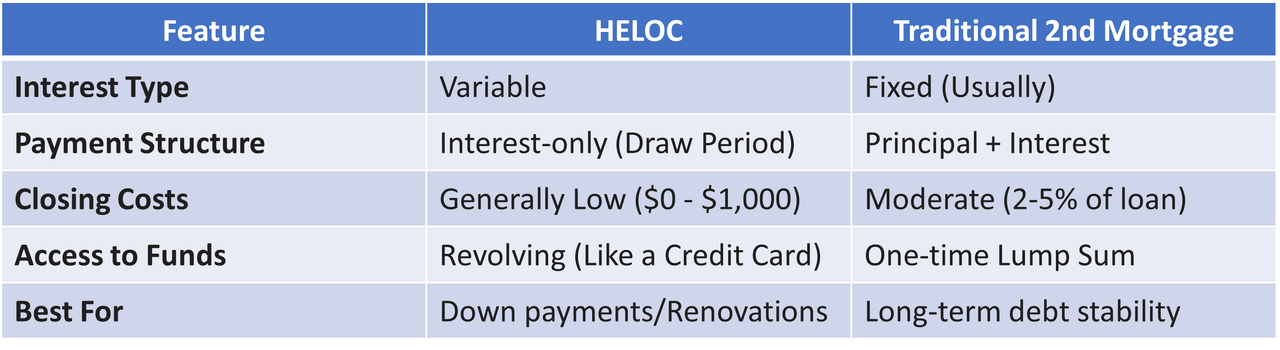

HELOC Basics

Loan Against Home Equity: Your credit limit is based on the appraised value of your home minus what you still owe on your primary mortgage.

Line of Credit vs. Lump Sum: You have the freedom to spend only what you need for a down payment or closing costs, leaving the rest of the credit line available for emergencies or renovations.

Interest-Only Draw Period: Most HELOCs offer a 10-year “draw period.” During this time, you typically only have to pay interest on the amount you’ve borrowed, which keeps initial monthly costs low while you manage a new second home.

Why Buyers Consider a HELOC for a Second Home Purchase

With the 2026 market showing signs of increased competition in the “second home” sector—driven by the continued normalization of remote work—buyers need to move fast. A HELOC provides “ready-to-go” capital that acts like cash in the eyes of a seller.

Financial Leverage & Timing

Using a HELOC allows you to maintain your liquidity. Instead of selling off stocks or dipping into a high-yield savings account (which may be earning 4-5% in today’s environment), you leverage the “dead equity” in your home. This strategy is particularly effective when you need to act quickly on a property listing before other buyers can secure traditional financing. It also allows you to bypass the need for a “home sale contingency” if you were planning to sell a different asset to fund the purchase.

Pros of Using a HELOC to Buy a Second Home

Leveraging your primary residence comes with distinct advantages that traditional second-home mortgages often lack:

Minimal Upfront Costs: HELOCs often have little to no closing costs. Many lenders in 2026 offer “no-cost” setups where they cover the appraisal and origination fees.

Borrow up to 85% CLTV: Most lenders allow a Combined Loan-to-Value (CLTV) of 80% to 85%. If your home is worth $1,000,000 and you owe $500,000, you could potentially access up to $350,000 in credit.

Tax Advantages: Per current IRS guidelines, the interest on a HELOC may be tax-deductible if the funds are used specifically to “buy, build, or substantially improve” the home that secures the loan.

Flexibility: You only pay interest on what you use. If you only need $50,000 for a down payment on a $250,000 condo, you aren’t forced to pay interest on a full $250,000 loan.

Cons & Risks of Using a HELOC for a Second Home

Despite the benefits, this strategy is not without significant risk. In the 2026 economy, borrowers must be wary of “rate creep” and equity volatility.

Variable Interest Rates: HELOCs are almost always tied to the Prime Rate. If the Federal Reserve raises rates to combat inflation, your HELOC payment will climb immediately.

Collateral Risk: Your primary home is the collateral. If you experience a financial hardship and cannot pay the HELOC, you risk losing the roof over your head.

Future Payment Shock: Once the 10-year draw period ends, the loan enters the “repayment period” (usually 20 years). At this point, you must pay both principal and interest, which can cause your monthly payment to double or even triple.

Rate Volatility & Market Conditions

Over the last 5 to 10 years, we have seen the Prime Rate move from near-zero to over 8%. While 2026 forecasts suggest a period of relative stability, a 2% increase in the Prime Rate can add significant stress to a household budget that is already managing two properties. Borrowers should always calculate their “break-even” point—the highest interest rate they could afford before the second home becomes a financial burden.

How Lenders Evaluate HELOC Usage

Securing a HELOC in 2026 is a more rigorous process than it was a decade ago. Lenders are looking for “pristine” borrowers who can weather economic shifts.

Credit Score: A FICO score of 720+ is typically required for the best rates, though some lenders will go down to 680 with higher interest margins.

Debt-to-Income (DTI): Most lenders want to see a DTI of 43% or lower. This calculation includes your primary mortgage, the new HELOC payment, and the projected costs of the second home (taxes, insurance, and HOA).

Home Equity: You usually need at least 15-20% equity remaining in the home after the HELOC is taken out.

Occupancy Type: Lenders will ask if the second home is a “vacation home” or an “investment property.” Investment properties often carry stricter requirements and slightly higher rates.

Smart Strategies for Using a HELOC to Buy Your Second Home

The Down Payment Bridge: Use the HELOC only for the 20% down payment. This allows you to avoid Private Mortgage Insurance (PMI) on your second home mortgage while keeping your cash reserves intact.

The “Fix and Refi”: Use the HELOC to buy a property that needs work. Once the renovations are complete and the value of the second home has increased, perform a “cash-out refinance” on the second home to pay off the HELOC on your primary home.

Aggressive Principal Reduction: During the 10-year draw period, don’t just pay the interest. Treat it like a fixed loan and pay down the principal monthly to reduce your long-term interest exposure.

HELOC vs. Traditional Second Mortgage

Real-World Example (Hypothetical)

magine a homeowner in 2026 with the following profile:

Primary Residence Value: $800,000

Current Mortgage: $400,000

Available Equity: $400,000

They find a beach cottage for $500,000. Instead of taking out a full $500,000 mortgage at 6.5%, they use their HELOC to pull $100,000 (20%) for a down payment. They then finance the remaining $400,000 with a traditional mortgage.

By using the HELOC, they avoided a “Jumbo” loan category (if applicable) and kept $100,000 in their brokerage account, which is currently yielding 8% annually. The “cost of capital” from the HELOC is offset by the “return on capital” from their investments.

What This Means for Buyers & Investors in 2026

The 2026 market is characterized by steady, if not explosive, growth. Rental demand remains high as many would-be buyers stay on the sidelines due to inventory shortages. For the savvy investor, using a HELOC to buy a second home is a way to capitalize on this rental demand.

However, keep an eye on the Tax Cuts and Jobs Act (TCJA) provisions, as tax laws regarding interest deductibility can shift. In 2026, the strategy is about precision: using just enough equity to secure the deal without over-leveraging your foundation.

Conclusion: Is a HELOC Right for You?

Leveraging your home equity to expand your real estate holdings is one of the fastest ways to build long-term wealth. A HELOC provides the speed and flexibility needed in a modern market, but it requires a disciplined repayment strategy and a keen eye on interest rate trends.

Before you tap into your equity, it is essential to have a professional evaluate your debt-to-income ratio and your long-term goals.

Would you like a personalized equity analysis to see how much you can borrow? Contact Level Mortgage today to explore HELOC options tailored to your second home goals.

Want personalized assistance? Visit our 'Contact Us' tab and leave your information with one of our experts.

About Us

A group of like-minded seasoned veterans came together to create a company with an employee-focused culture. A culture that values its members both personally and professionally and a company built on the idea that the customer comes first!

We do not share data with third parties for marketing/promotional purposes.

By submitting your phone number to Level Mortgage, you are authorizing a representative of our company to send you text messages and notifications. Message frequency may vary. Message/data rates apply. Reply STOP to unsubscribe to a message sent from us, and HELP to receive help.

-(10).jpg)