Adjustable-Rate Loans Explained: How They Work & When to Get One

Navigating the mortgage landscape in 2026 requires more than just checking the daily interest rates. It involves understanding the tools available to maximize your purchasing power and align your financing with your lifestyle goals. One of the most misunderstood yet potentially powerful tools in a borrower’s arsenal is the Adjustable-Rate Mortgage (ARM). While fixed-rate loans are the industry standard, ARMs offer unique features that may serve specific financial strategies. This guide will help you understand how these loans function and how to determine if one is right for your unique situation.

What Is an Adjustable-Rate Mortgage (ARM)?

An Adjustable-Rate Mortgage is a home loan with an interest rate that can fluctuate over the life of the loan. Unlike a fixed-rate mortgage, where your interest rate and principal and interest payments remain constant for the entire term, an ARM features an initial period of stability followed by a period where the rate adjusts based on market conditions.

Lenders offer ARMs because they provide flexibility for borrowers who do not plan to stay in their homes for 30 years. The rate on an ARM is typically tied to an index, which is a benchmark interest rate that reflects general market conditions. When you add a margin, which is a set percentage determined by the lender, you arrive at the fully indexed rate that determines your payment during the adjustment period.

How Adjustable-Rate Mortgages Work

Understanding an ARM requires looking beyond the initial rate. These loans are built on a specific structure that dictates when and how your payment changes.

The Initial Fixed-Rate Period

Every ARM has an initial period where the interest rate is fixed. This is often represented by two numbers, such as a 5/1 ARM or a 7/1 ARM. The first number represents the years the rate remains fixed. The second number indicates how often the rate can adjust after that period ends. For example, in a 5/1 ARM, your rate is locked for five years. After that, the rate can adjust once every year.

The Adjustment Period

Once the initial fixed period expires, the loan enters the adjustment period. During this time, the lender recalculates your interest rate based on current market indexes. If market rates have risen, your payment may increase. Conversely, if rates have fallen, your payment could decrease. This period continues for the remainder of the loan term, which is typically 30 years.

Rate Caps and Borrower Protections

To protect borrowers from wild fluctuations, ARMs include rate caps.

Initial Adjustment Cap: Limits how much the rate can increase the first time it adjusts.

Periodic Cap: Limits how much the rate can increase from one adjustment period to the next.

Lifetime Cap: Sets a maximum limit on how high the interest rate can rise over the entire life of the loan.

These caps are vital safeguards that prevent your monthly payment from becoming unexpectedly unmanageable.

Why Some Buyers Choose ARMs in 2026

In 2026, the housing market presents unique challenges regarding affordability. Mortgage Rate Trends Report indicates that while rates have stabilized, they remain at a level that pressures the monthly budgets of many homebuyers. Consequently, borrowers are looking for financing options that provide a lower entry point.

Many buyers are exploring ARMs because the initial interest rate is often lower than the rate offered on a traditional fixed-rate loan. This can result in lower monthly payments, which helps borrowers qualify for a higher loan amount. As noted in Housing Affordability Report, strategic financing is becoming a key component for homebuyers looking to enter competitive markets without overextending their monthly cash flow.

Potential Benefits of an Adjustable-Rate Mortgage

Lower Initial Interest Rates

The primary draw of an ARM is the initial lower interest rate. For buyers who plan to move within a few years, this can lead to substantial savings.

Lower Monthly Payments

Lower rates translate directly to lower monthly obligations. This extra breathing room in your budget can be used to pay down other high-interest debt or save for future home maintenance.

Increased Buying Power

Because your initial monthly payment is lower, your debt-to-income ratio may look more favorable to a lender. This can allow you to purchase a home that might have been out of reach under a fixed-rate loan.

Savings for Short-Term Homeowners

If you know you will be in the home for less than the duration of the fixed period, an ARM can be a mathematically superior choice. You capture the lower rate during your entire ownership period and sell or refinance before the first adjustment ever occurs.

Risks Homebuyers Should Understand

While ARMs offer advantages, they carry inherent risks that should not be overlooked.

Future Payment Increases

The most significant risk is the uncertainty of future payments. If market rates rise significantly by the time your adjustment period begins, your monthly housing expense could climb.

Interest Rate Volatility

Market conditions can change rapidly. ARM Market Statistics shows that while ARMs are a stable tool, they are still subject to broader economic shifts that can impact interest rates unexpectedly.

Budgeting Challenges

For homeowners who prefer predictable finances, the variable nature of an ARM can cause stress. It requires a more disciplined approach to financial planning compared to a fixed-rate loan.

When an ARM May Make Sense

An ARM is often a strategic choice rather than a risky gamble. It may make sense if:

You plan to relocate: If you are in a career that requires frequent moves, a 5/1 or 7/1 ARM allows you to take advantage of lower rates for the short time you plan to own the home.

You expect income growth: If you are an early-career professional expecting your salary to increase significantly over the next few years, an ARM can help you manage your budget now, with the peace of mind that you will be able to handle potential payment increases later.

You plan to refinance: If you intend to refinance into a fixed-rate mortgage within a few years, an ARM can bridge the gap.

For those who need long-term stability, a Fixed-Rate Mortgage Guide is generally the safer recommendation. Retirees or those on fixed incomes should carefully consider the risks of payment fluctuations before choosing an ARM.

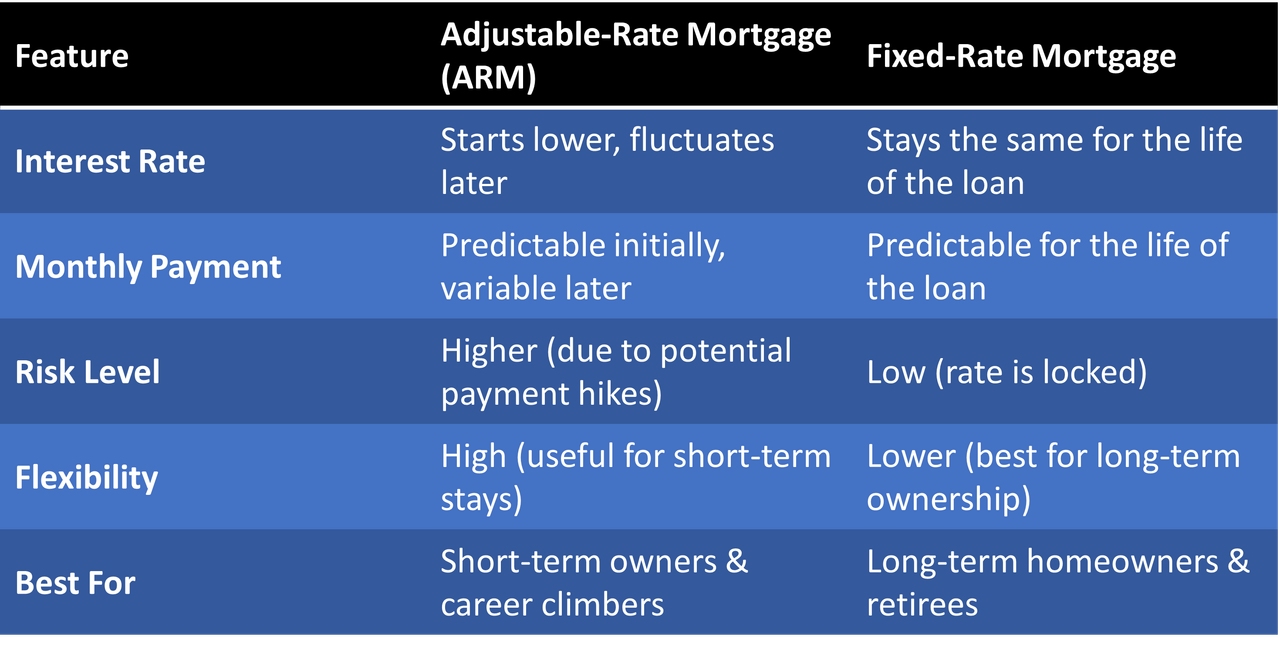

ARM vs Fixed Mortgage: A Side-by-Side Comparison

How Level Mortgage Helps Borrowers Choose the Right Loan

At Level Mortgage, we do not believe in one-size-fits-all financing. We act as your mortgage planners, not just loan processors. We perform comprehensive loan comparison analysis to show you exactly how different products will affect your monthly budget and long-term wealth.

Whether you are applying for Mortgage Pre-Approval or just beginning to navigate the Home Buying Process, our goal is to provide clarity. We want you to feel confident that your mortgage is a strategic asset, not a burden. From evaluating Loan Programs to guiding you through our First-Time Homebuyer Guide, we are here to ensure you understand every aspect of your financial commitment.

Final Thoughts

Adjustable-rate mortgages are sophisticated financial instruments that, when used strategically, can provide significant advantages in affordability and purchasing power. However, they are not suitable for every borrower. The decision to choose an ARM should be based on your unique timeline, your financial flexibility, and your tolerance for market changes. As we look at the Mortgage Industry Forecast for the remainder of 2026, it is clear that borrowers who take the time to evaluate their options will be in the best position to succeed. Connect with Level Mortgage today to begin your loan comparison and find the financing strategy that aligns with your future.

Want personalized assistance? Visit our 'Contact Us' tab and leave your information with one of our experts.

About Us

A group of like-minded seasoned veterans came together to create a company with an employee-focused culture. A culture that values its members both personally and professionally and a company built on the idea that the customer comes first!

We do not share data with third parties for marketing/promotional purposes.

By submitting your phone number to Level Mortgage, you are authorizing a representative of our company to send you text messages and notifications. Message frequency may vary. Message/data rates apply. Reply STOP to unsubscribe to a message sent from us, and HELP to receive help.