How to Finance a New Construction Condo Before Completion

Buying a home that has not yet been built is an exciting prospect, especially in high-demand markets like South Florida. It offers the chance to secure a modern residence at today’s prices while the building rises from the ground. However, the financial path for a pre-construction unit is fundamentally different from buying an existing home.

Because the property does not yet exist as physical collateral, you cannot simply walk into a bank and get a standard mortgage on day one. Navigating this process requires a clear understanding of deposit phases, long-term credit stability, and the specific lending rules of 2026.

Why Buying Before Completion Is Different

When you buy a resale home, the transaction usually closes within thirty to sixty days. The property is inspected, appraised, and the mortgage is funded immediately. With a new construction condo, the timeline often stretches from one to four years.

Property Use Classification

This gap creates a unique set of challenges. The property cannot be used as collateral for a traditional mortgage until it receives a Certificate of Occupancy. This means the lender is essentially approving a loan for an asset that is not yet fully realized.

The Shift in Market Conditions

Furthermore, the market conditions and your personal financial situation may change between the time you sign the contract and the day you finally move in. While this involves more moving parts, it also provides the opportunity for significant equity growth before you even make your first mortgage payment.

Understanding the Two-Phase Financing Process

Financing a pre-construction condo is essentially a two-phase journey. You must treat the initial purchase and the final loan as two distinct financial events.

Phase One: The Deposit Phase

In the first phase, you are responsible for the deposit structure required by the developer. This is typically handled using your own liquid capital, proceeds from a current home sale, or personal lines of credit. Lenders do not typically provide mortgage funds at this stage.

Phase Two: The Mortgage Phase

The second phase is the mortgage phase. This occurs when the building is nearing completion. Only at this point does a traditional lender step in to provide the long-term financing. According to recent industry data, many buyers find themselves in a position where they must manage their liquidity for several years before the actual loan is finalized.

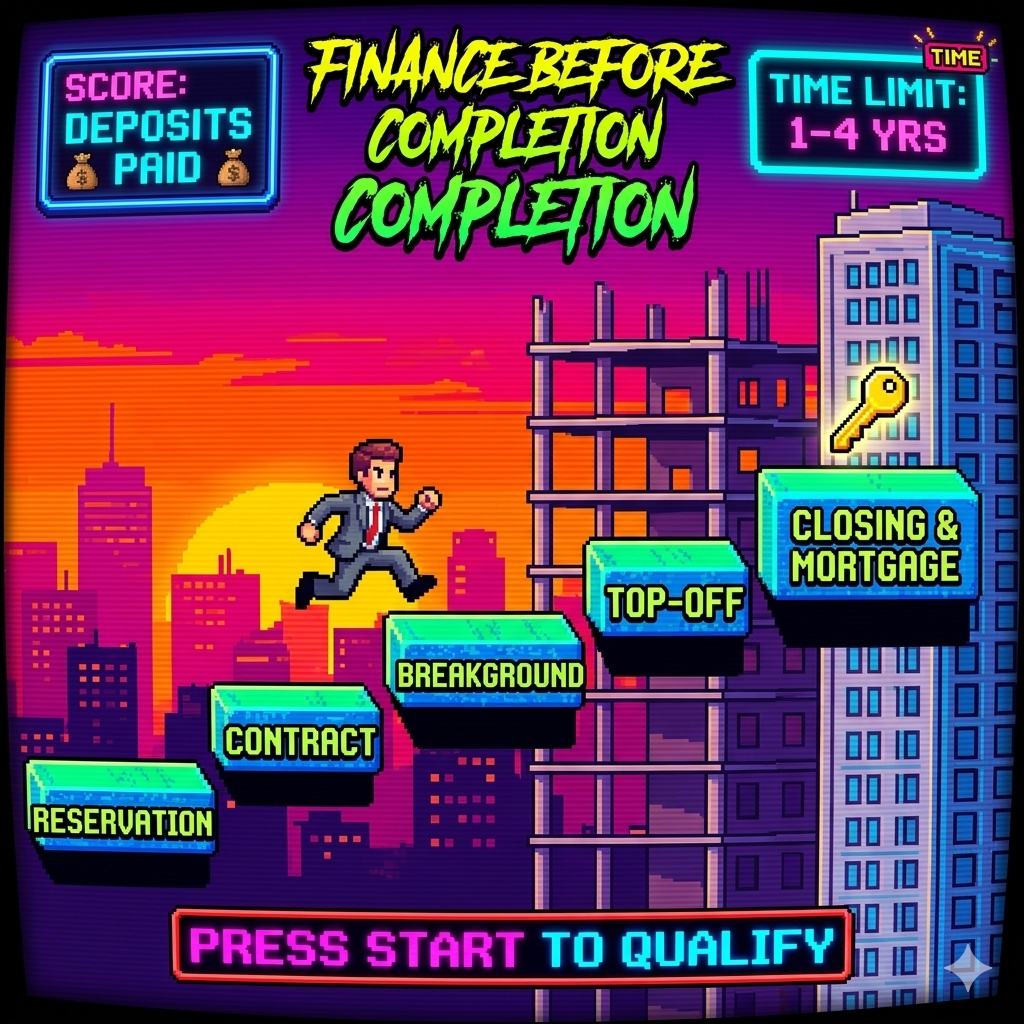

Typical Deposit Structure in 2026

Developers use your deposits to help fund the construction and prove the viability of the project to their own commercial lenders. Based on trusted mortgage reports, the standard deposit structure in 2026 has remained fairly consistent for premier developments.

10% at Reservation: This is the initial “good faith” deposit to hold the specific unit.

10% at Contract: Due when you sign the official purchase and sale agreement.

10% at Groundbreaking: Paid when the developer officially starts construction.

10% at Top-off: This occurs when the building reaches its highest structural point.

60% at Closing: The remaining balance is due when the unit is complete, usually covered by your mortgage.

Planning for Liquidity

This structure means you must have significant cash available early in the process. Planning for this liquidity is essential to ensure you do not default on your contract as the building reaches its milestones.

How to Qualify for the Mortgage at Closing

One of the most common misconceptions is that getting “pre-approved” at the time of the contract means you are set for the next three years. In reality, you must re-qualify for your mortgage as the building nears completion.

The Re-Qualification Reality

Lenders will perform a fresh review of your credit score, income stability, and debt-to-income ratio. Recent lending guidelines indicate that a credit score of 680 or higher is generally expected, though 720 or higher often yields the most competitive rates.

Avoiding Financial Major Changes

If you take on new debt, such as a car loan, or experience a significant change in employment during the construction years, it could jeopardize your final approval. Maintaining financial stability is the best strategy for a successful closing.

Condo Approval and Financing Challenges

Even if your personal finances are perfect, the condo project itself must meet specific lender requirements. Lenders look at the health of the entire building, not just your unit.

Warrantable vs. Non-Warrantable

Recent updates to condo financing rules in 2026 emphasize the importance of owner occupancy and financial reserves. Generally, a project should have an owner-occupancy threshold of around 50% to be considered warrantable by major agencies.

HOA Reserves and Risk

Additionally, the Homeowners Association (HOA) must typically allocate at least 10% of its budget to a reserve fund. If a project is deemed non-warrantable, perhaps because one entity owns too many units or the commercial space exceeds certain limits, you may need alternative financing. These loans often require a 20% to 25% down payment and carry interest rates that are 0.5% to 1.5% higher than standard programs.

Strategies to Reduce Risk Before Completion

Because of the long timeline, risk management is a priority. You want to ensure that the excitement of a new home isn’t overshadowed by financial stress at the finish line.

Locking Interest Rates

One strategy is to keep a close eye on interest rates. While most lenders cannot lock a rate for three years, some offer specialized long-term lock options for a fee. This can protect you if rates rise significantly during the construction period.

Expert Guidance on Contracts

You should also work closely with an experienced lender who understands developer contracts. Some contracts have specific clauses regarding your right to find outside financing versus using the developer’s preferred lender. Understanding these nuances early can save you thousands in closing costs.

Benefits of Buying Pre-Construction

Despite the complexity, the rewards can be substantial. Buying early often allows you to secure “lower entry pricing” compared to what the units will cost once the building is finished.

As construction progresses, the value of your contract often appreciates. It is not uncommon for buyers to have significant equity in their units before they ever move in. Additionally, buying before completion gives you the best choice of floor plans, views, and interior finishes, allowing you to customize your living space to your exact preferences.

How Level Mortgage Helps You Navigate the Process

At Level Mortgage, we specialize in the intricate world of new construction. We don’t just look at where you are today, we help you plan for where you will be when the building is finished.

Our team assists in structuring a financing strategy years in advance. We help you understand whether a project is warrantable and what your options are if it isn’t. We also guide you through the re-qualification process, ensuring your credit and income remain in the best possible shape for that final closing day. By acting as a strategic advisor, we turn a complex construction timeline into a clear path toward your new home.

Want personalized assistance? Visit our 'Contact Us' tab and leave your information with one of our experts.

About Us

A group of like-minded seasoned veterans came together to create a company with an employee-focused culture. A culture that values its members both personally and professionally and a company built on the idea that the customer comes first!

We do not share data with third parties for marketing/promotional purposes.

By submitting your phone number to Level Mortgage, you are authorizing a representative of our company to send you text messages and notifications. Message frequency may vary. Message/data rates apply. Reply STOP to unsubscribe to a message sent from us, and HELP to receive help.

How to Buy Your First Home in Florida: Step-by-Step Guide for 2025

If you’re a first-time homebuyer in Florida, partnering with Level Mortgage can be your smartest move. With personalized service, fast closings, and access to powerful assistance programs, Level Mortgage simplifies the journey from dream to doorstep.

Understanding the Florida Housing Market in 2025

Florida’s real estate market offers unique opportunities and challenges. As of mid-2025, the statewide median home price has dropped nearly 5%, making it a favorable time for buyers. However, navigating flood zones, insurance requirements, and competitive bidding can be daunting without expert guidance.

That’s where Level Mortgage shines. Founded by Angelo Lamas, this Florida-based brokerage is known for speed, transparency, and tailored loan solutions. With a 5.0 rating across platforms like Experience.com, Level Mortgage has earned trust from first-time buyers, veterans, and real estate professionals alike.

Step-by-Step Guide to Buying Your First Home with Level Mortgage

Level Mortgage offers fast pre-approvals, often within 24–48 hours. Pre-approval helps you:

– Know your budget

– Strengthen your offer

– Speed up closing

Clients rave about the team’s responsiveness: “They worked super fast—even late hours—to make sure I could close on my house.” — Carlos D

3. Explore Assistance Programs

Level Mortgage specializes in Florida’s Hometown Heroes Program, which provides up to $35,000 in down payment and closing cost assistance for eligible buyers. This includes teachers, healthcare workers, law enforcement, and other frontline professionals.

Other programs include:

– Florida Housing First-Time Homebuyer Program

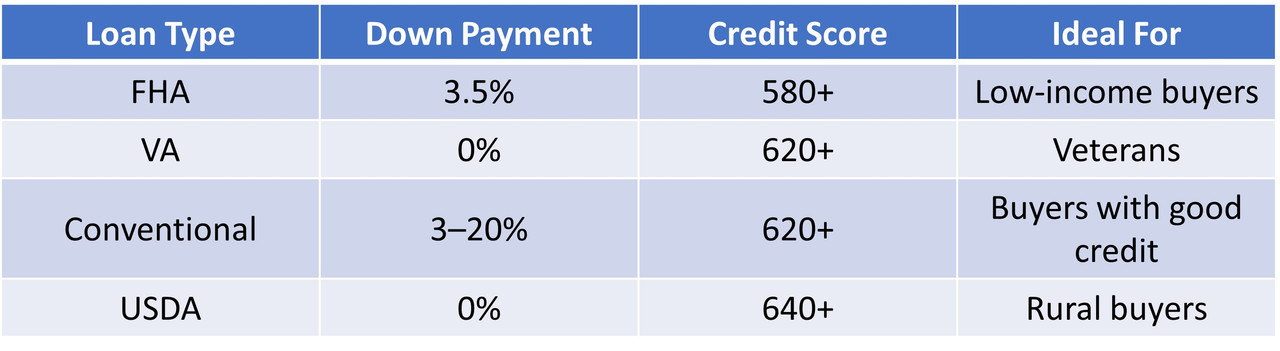

– FHA Loans (3.5% down payment)

– VA Loans (0% down for veterans)

– USDA Loans (0% down in rural areas)

Level Mortgage helps you navigate these options to maximize savings.

4. Choose the Right Loan

Level Mortgage tailors loan terms to your financial profile. Whether you’re self-employed, have student debt, or need flexible terms, they’ll match you with the best product.

With Level Mortgage’s pre-approval in hand, your offer stands out. Their team works closely with agents to ensure fast communication and document delivery.

7. Close Quickly

Level Mortgage is known for expedited closings, often beating industry averages. Their transparent fee structure means no surprises at closing, as noted by client Idalis L: “Tomás Lamas explained all disclosures in detail and helped me understand every fee and payment.”

Why Level Mortgage Is the Right Choice

– Fast Closings: Ideal for competitive markets

– Personalized Service: Loans tailored to your financial goals

– Transparent Communication: Clear disclosures and fee breakdowns

– Expertise in Assistance Programs: Maximize your benefits

– Top Reviews: 5.0 rating across platforms

Final Thoughts

Buying your first home in Florida doesn’t have to be overwhelming. With Level Mortgage, you gain a partner who understands the local market, prioritizes your financial well-being, and delivers results with speed and clarity. Whether you’re a teacher, nurse, or recent graduate, Level Mortgage helps you unlock the door to homeownership.

Ready to start your journey? Reach out to Level Mortgage and let Angelo Lamas and his team guide you home.

Want personalized assistance? Visit our 'Contact Us' tab and leave your information with one of our experts.

About Us

A group of like-minded seasoned veterans came together to create a company with an employee-focused culture. A culture that values its members both personally and professionally and a company built on the idea that the customer comes first!

We do not share data with third parties for marketing/promotional purposes.

By submitting your phone number to Level Mortgage, you are authorizing a representative of our company to send you text messages and notifications. Message frequency may vary. Message/data rates apply. Reply STOP to unsubscribe to a message sent from us, and HELP to receive help.