Buying a home is one of the most significant financial decisions most people will ever make. Yet many potential buyers choose to “wait for the right time,” hoping for lower prices or better mortgage rates. But in today’s evolving real estate landscape, waiting often comes with a real financial cost.

Recent data from late 2025 and early 2026 shows that affordability is shifting, mortgage rates are adjusting, and home prices continue to evolve—making timing more important than ever. Below is a comprehensive breakdown of what waiting could cost you based on the latest market information.

Inventory increased in many major metros, giving buyers more options.

Home prices stabilized but did not significantly decline.

Mortgage rates remained elevated compared to pre‑2022 levels.

Homes stayed on the market longer, giving buyers more negotiation power.

Even with these improvements, affordability remained a challenge. Zillow reported that by the end of 2025, mortgage payments were still consuming 32.6% of the median household income, despite being $177 lower than their October 2023 peak.

2. What’s Changing in 2026?

The 2026 housing market is expected to bring slightly better conditions for buyers. Zillow forecasts that 20 of the 50 largest U.S. metros will become affordable by the end of 2026, the highest number since 2022.

2026 Forecast Highlights:

Home values are expected to rise 1.9% in 2026—not a crash, but a moderate increase.

More inventory is entering the market, especially new construction.

Some cities may even see price declines due to increased supply.

However, even with improved affordability, waiting may still cost buyers more in the long run due to rising home values and the compounding effect of mortgage interest.

3. The Real Cost of Waiting: Price Appreciation

Even modest price increases can significantly impact affordability.

Example:

If a $400,000 home appreciates by Zillow’s projected 1.9% in 2026, the same home would cost:

400,000×1.019=407,600

That’s $7,600 more in just one year.

If appreciation continues at similar rates, waiting two years could cost buyers $15,000–$20,000 or more—before even factoring in mortgage interest.

4. Mortgage Rates: The Silent Cost Multiplier

Mortgage rates are one of the biggest factors affecting the cost of waiting.

While rates have eased slightly from their 2023–2024 highs, they remain elevated historically. Even a 0.5% increase in mortgage rates can add tens of thousands of dollars in interest over the life of a loan.

Impact of a 0.5% Rate Increase on a $400,000 Loan:

Difference:

+$133/month

+$48,000 over 30 years

Even if home prices stay flat, rising rates alone can make waiting significantly more expensive.

5. Inventory Growth Doesn’t Always Mean Lower Prices

CNBC reported that by late 2025, homes were sitting longer on the market and builders were offering discounts in some areas due to increased supply. However, this does not guarantee widespread price drops.

Why?

New construction often targets higher‑income buyers.

Demand remains strong due to demographic pressure (Millennials + Gen Z).

Many homeowners are still “locked in” with ultra‑low pre‑2022 mortgage rates, limiting resale inventory.

This means that while buyers may have more choices, prices are unlikely to fall dramatically nationwide.

6. Affordability Is Improving—But Slowly

Zillow’s January 2026 report shows that affordability is improving due to:

Slower price growth

Slightly lower mortgage rates

Rising incomes

However, affordability improvements do not necessarily mean homes will become cheaper. Instead, they mean buyers may be better able to handle current prices.

Waiting for a “big crash” is not supported by current data. In fact, Zillow expects home values to increase in 41 of the 50 largest metros in 2026.

7. The Opportunity Cost of Delayed Homeownership

Waiting to buy a home also means missing out on:

Equity Growth

If a home appreciates even 2% annually, a $400,000 home gains:

400,000×0.02=8,000 per year

That’s $40,000 in equity over five years.

Tax Benefits

Homeowners may deduct:

Mortgage interest

Property taxes

Certain closing costs

Renters receive none of these benefits.

Fixed Housing Costs

Rent typically increases 3–7% per year in many markets. A fixed mortgage payment does not.

8. Florida Market Considerations

While the data above reflects national trends, Florida has unique dynamics:

Strong population growth

High demand from out‑of‑state buyers

Limited land in coastal metros

Strong new construction pipeline

These factors often lead to above‑average price appreciation, making waiting even more costly for Florida buyers.

Final Thoughts: Should You Wait to Buy a Home?

Based on late‑2025 and early‑2026 data, waiting to buy a home can cost you through:

Higher home prices

Higher mortgage rates

Lost equity

Lost tax benefits

Rising rents

While the market is becoming more balanced, the long‑term trend still points toward rising home values and steady demand.

For most buyers—especially in high‑growth states like Florida—the cost of waiting outweighs the potential benefits.

If you’re financially ready, 2026 may be one of the best windows to buy before prices and rates shift again.

Want personalized assistance? Visit our 'Contact Us' tab and leave your information with one of our experts.

About Us

A group of like-minded seasoned veterans came together to create a company with an employee-focused culture. A culture that values its members both personally and professionally and a company built on the idea that the customer comes first!

We do not share data with third parties for marketing/promotional purposes.

By submitting your phone number to Level Mortgage, you are authorizing a representative of our company to send you text messages and notifications. Message frequency may vary. Message/data rates apply. Reply STOP to unsubscribe to a message sent from us, and HELP to receive help.

How to Prepare for Your First Consultation with a Mortgage Professional

Preparing for your first mortgage consultation is one of the most important steps in the homebuying process. Whether you’re purchasing your first home, relocating to Florida, or upgrading your current property, arriving prepared can dramatically improve your loan options, speed up approval, and help you understand your true buying power. According to industry guidance, the first consultation is designed to help you understand your options—not to obligate you to a loan application.

This guide breaks down everything you need to bring, what to expect, and how to position yourself for success in Florida’s competitive real estate market.

Why Your First Mortgage Consultation Matters

Your initial meeting with a mortgage professional sets the tone for your entire homebuying journey. It helps you:

Understand your loan options

Determine your purchasing power

Identify potential credit or financial issues early

Build a strategy for navigating Florida’s fast‑moving housing market

Mortgage experts emphasize that preparing ahead of time leads to a smoother experience from start to finish.

1. Know Your Homeownership Goals

Before your consultation, define what you want to accomplish. This helps the mortgage professional tailor recommendations.

Questions to Ask Yourself

Are you a first‑time buyer or repeat buyer?

Are you upsizing, downsizing, or relocating?

What Florida cities or counties are you targeting?

What is your ideal monthly payment?

How long do you plan to stay in the home?

Florida’s market is diverse—Miami, Tampa, Orlando, and Jacksonville each have different price points and lending dynamics. Knowing your goals helps your lender match you with the right loan program.

The average U.S. credit score is around 715 (FICO).

FHA loans allow scores as low as 580, but with higher costs.

Conventional loans typically require 620+.

If your score is lower than expected, your mortgage professional can help you create a plan to improve it before applying.

4. Understand Your Debt‑to‑Income Ratio (DTI)

DTI is a key metric lenders use to determine affordability.

Typical DTI Requirements

Conventional loans: up to 45%

FHA loans: up to 57% with strong compensating factors

VA loans: flexible but typically under 41%

Reducing debt before your consultation can significantly improve your loan options.

5. Research Florida Market Conditions

Florida’s real estate market remains one of the most active in the U.S. Understanding local trends helps you prepare realistic expectations.

Key Florida Market Facts (2025–2026)

Florida remains a top‑3 state for population growth.

Median home prices increased between 3%–6% in major metros year‑over‑year.

Inventory remains tight in coastal counties, increasing competition.

Your mortgage professional will help you understand how these trends affect your buying power.

6. Prepare Questions for Your Mortgage Professional

A consultation is a two‑way conversation. Bring questions that help you understand your options.

Smart Questions to Ask

What loan programs do I qualify for?

What down payment options are available?

What interest rate range should I expect?

What are the estimated closing costs?

How long does the approval process take?

Are there Florida‑specific programs I can use (Hometown Heroes, first‑time buyer grants, etc.)?

7. Understand What Happens During the Consultation

According to mortgage industry guidance, your consultation will typically include:

A review of your financial documents

A discussion of your goals and timeline

A preliminary assessment of your loan eligibility

An explanation of loan types (FHA, VA, USDA, Conventional, Jumbo)

A breakdown of estimated payments and costs

This meeting is designed to empower you with information—not pressure you into a loan.

8. Avoid Common Mistakes Before Your Consultation

Do NOT:

Make large purchases

Open new credit accounts

Transfer large sums between accounts

Change jobs without discussing it with your lender

These actions can negatively impact your loan eligibility.

9. Prepare for a Competitive Florida Market

Florida’s housing market is fast‑paced. Being prepared gives you an advantage.

Competitive Advantages You Gain by Preparing

Faster pre‑approval

Stronger offers

Better negotiation power

Ability to lock rates quickly

In markets like Miami‑Dade, Hillsborough, and Orange County, homes often receive multiple offers within days.

10. Final Checklist Before Your Consultation

Bring:

Financial documents

Credit report

List of questions

Notes about your goals

Proof of funds for down payment

Be Ready To Discuss:

Budget

Employment history

Savings

Timeline

Preferred loan type

Conclusion

Preparing for your first consultation with a mortgage professional is one of the smartest steps you can take as a Florida homebuyer. With the right documents, clear goals, and an understanding of your financial picture, you’ll walk into your meeting confident and ready to take the next step toward homeownership.

Want personalized assistance? Visit our 'Contact Us' tab and leave your information with one of our experts.

About Us

A group of like-minded seasoned veterans came together to create a company with an employee-focused culture. A culture that values its members both personally and professionally and a company built on the idea that the customer comes first!

We do not share data with third parties for marketing/promotional purposes.

By submitting your phone number to Level Mortgage, you are authorizing a representative of our company to send you text messages and notifications. Message frequency may vary. Message/data rates apply. Reply STOP to unsubscribe to a message sent from us, and HELP to receive help.

Using a HELOC to Pay Off Credit Card Debt: Is It Right for You?

Florida homeowners are increasingly turning to Home Equity Lines of Credit (HELOCs)as a way to manage high-interest credit card debt. With credit card APRs averaging over 20% nationally in 2025, the appeal of tapping into home equity—where rates are often in the 6–8% range—is obvious. But is this strategy right for you? Let’s break down the numbers, risks, and opportunities.

What Is a HELOC?

A HELOC is a revolving line of credit secured by your home’s equity.

Unlike a lump-sum home equity loan, HELOCs allow flexible borrowing and repayment, similar to a credit card but with lower rates.

Your home serves as collateral, meaning missed payments could lead to foreclosure.

Mortgage balances account for $13.07 trillion, while HELOC balances rose by $11 billion, marking the 14th consecutive quarterly increase.

Credit card debt is surging, with balances exceeding $1.3 trillion nationwide, driven by inflation and consumer spending.

In Florida, where housing values have risen sharply post-pandemic, homeowners often have significant equity available. This makes HELOCs an attractive option for debt consolidation.

Why Consider a HELOC for Credit Card Debt?

1. Lower Interest Rates

Average credit card APR: 20–24%

Average HELOC rate: 6–8%

Example: $20,000 in credit card debt at 22% costs about $4,400 annually in interest. A HELOC at 7% would reduce that to $1,400 annually, saving $3,000 per year.

2. Flexible Repayment

HELOCs allow interest-only payments during the draw period, easing short-term cash flow.

Borrowers can pay down principal aggressively when finances improve.

3. Potential Tax Benefits

Interest on HELOCs may be tax-deductible if funds are used for home improvements. However, using it for debt consolidation typically does not qualify.

Risks and Trade-Offs

1. Your Home Is Collateral

Defaulting on a HELOC can lead to foreclosure.

Unlike credit card debt, which is unsecured, HELOC debt ties directly to your property.

2. Variable Interest Rates

HELOCs often have adjustable rates. If rates rise, your payments could increase significantly.

While Fed rate cuts in 2025 have lowered HELOC rates to the mid-6% range, future hikes could reverse this trend.

3. Closing Costs and Fees

HELOCs may include appraisal fees, annual fees, and closing costs.

These can offset some of the interest savings if not carefully managed.

4. Discipline Required

Paying off credit cards with a HELOC only works if you stop accumulating new credit card debt.

Otherwise, you risk doubling your debt load—secured and unsecured.

Florida-Specific Considerations

Rising Home Values: Florida’s median home price has increased more than 40% since 2020, giving homeowners substantial equity to tap.

High Credit Card Usage: Florida ranks among the top states for average credit card balances, making HELOCs a popular consolidation tool.

Hurricane Risk: Insurance costs and property risks in Florida can complicate HELOC eligibility and affordability.

Alternatives to HELOCs

Balance Transfer Credit Cards: Introductory 0% APR offers can provide short-term relief but usually last only 12–18 months.

Personal Loans: Fixed-rate loans may offer predictable payments without risking your home.

Debt Management Plans: Nonprofit credit counseling agencies can negotiate lower rates with creditors.

Is It Right for You?

A HELOC can be a smart move if:

You have substantial home equity.

You’re disciplined enough to avoid new credit card debt.

You can handle potential rate fluctuations.

You understand the risk of foreclosure.

It may not be right if:

Your income is unstable.

You’re already struggling with mortgage payments.

You’re prone to overspending on credit cards.

Conclusion

Using a HELOC to pay off credit card debt can save thousands in interest and simplify repayment. But it’s not a one-size-fits-all solution. For Florida homeowners, where equity is abundant but risks like hurricanes and insurance costs loom large, the decision requires careful consideration.

Want personalized assistance? Visit our 'Contact Us' tab and leave your information with one of our experts.

About Us

A group of like-minded seasoned veterans came together to create a company with an employee-focused culture. A culture that values its members both personally and professionally and a company built on the idea that the customer comes first!

We do not share data with third parties for marketing/promotional purposes.

By submitting your phone number to Level Mortgage, you are authorizing a representative of our company to send you text messages and notifications. Message frequency may vary. Message/data rates apply. Reply STOP to unsubscribe to a message sent from us, and HELP to receive help.

Will Home Prices Drop in Florida? 2026 Real Estate Market Trends Explained

Florida’s real estate market has always been dynamic, shaped by migration trends, weather risks, and national economic conditions. As we move into 2026, many buyers and sellers are asking the same question: Will home prices drop? To answer this, let’s break down the latest data, regional variations, and the broader economic forces at play.

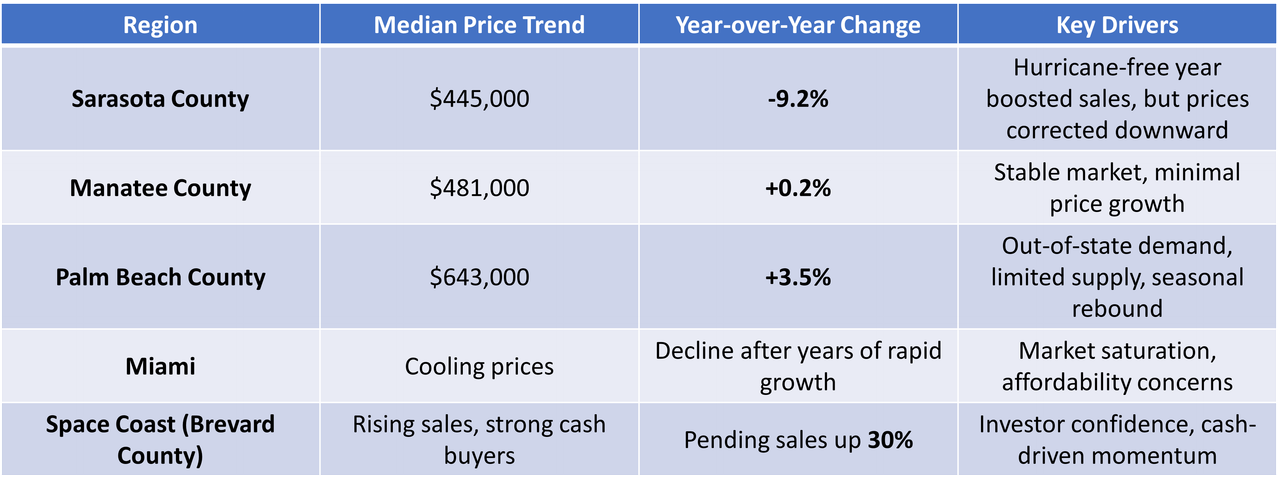

– Longer Time on Market: Homes now average 83 days on market, up from 70 days last year, signaling slower demand.

Factors Supporting Price Stability

Strong Migration: Florida continues to attract new residents, retirees, and investors, sustaining demand.

Cash Buyers:In areas like the Space Coast, cash purchases surged, insulating the market from mortgage rate fluctuations.

Mortgage Rate Relief: Slight declines in rates (from 6.64% to ~6%) could re-energize buyers in 2026.

Regional Resilience: Counties like Palm Beach and Manatee show steady or rising prices, proving that not all markets are weakening.

2026 Outlook: A “Two-Speed Market”

Experts describe the U.S. housing market as entering a “two-speed” phase:

– Growth Regions: Areas with strong migration (Palm Beach, Space Coast) will likely see modest price increases.

– Correction Regions: Overheated markets (Miami, Sarasota) may continue to decline or flatten.

Florida’s market is unlikely to “crash.” Instead, expect regional divergence: some counties will cool, while others remain competitive.

Key Takeaways for Buyers and Sellers

Experts describe the U.S. housing market as entering a “two-speed” phase:

– Growth Regions: Areas with strong migration (Palm Beach, Space Coast) will likely see modest price increases.

– Correction Regions: Overheated markets (Miami, Sarasota) may continue to decline or flatten.

Florida’s market is unlikely to “crash.” Instead, expect regional divergence: some counties will cool, while others remain competitive.

Conclusion

So, will home prices drop? The answer is nuanced. Yes, in some regions—Sarasota and Miami are already seeing declines. No, in others—Palm Beach and the Space Coast continue to rise. Florida’s housing market in 2026 will be defined by regional divergence, inventory growth, and affordability pressures.

For buyers, this means opportunity. For sellers, it means adjusting expectations. And for the market overall, it means a shift toward balance after years of volatility.

Want personalized assistance? Visit our 'Contact Us' tab and leave your information with one of our experts.

About Us

A group of like-minded seasoned veterans came together to create a company with an employee-focused culture. A culture that values its members both personally and professionally and a company built on the idea that the customer comes first!

We do not share data with third parties for marketing/promotional purposes.

By submitting your phone number to Level Mortgage, you are authorizing a representative of our company to send you text messages and notifications. Message frequency may vary. Message/data rates apply. Reply STOP to unsubscribe to a message sent from us, and HELP to receive help.

5 Expert Tips to Close Your Mortgage Loan Faster (Plus Bonus Strategies)

Want to close your mortgage loan faster? These 5 expert-backed tips—plus bonus strategies—can help you speed up the process, save money, and secure your dream home sooner

Closing a mortgage loan can feel like navigating a maze—paperwork, approvals, inspections, and deadlines. But with the right strategies, you can streamline the process and avoid costly delays. Whether you’re a first-time buyer or refinancing, here are five proven tips to help you close your mortgage loan faster, along with bonus strategies to give you an edge. This guide is brought to you in partnership with Level Mortgage, a trusted name in the mortgage lending space.

Get Pre-Approved, Not Just Pre-Qualified

Pre-approval is a game-changer. Unlike pre-qualification, which is based on self-reported financials, pre-approval involves a lender verifying your income, assets, credit score, and debt-to-income ratio. This gives you a realistic budget and shows sellers you’re serious.

– Level Mortgage’s online portal allows real-time communication and uploads, keeping the process moving.

Schedule Your Appraisal and Inspection ASAP

Appraisals and inspections are often bottlenecks. Book them early to avoid delays:

– Appraisals can take 7–10 business days depending on your market.

– If issues arise during inspection, you’ll need time to negotiate repairs or credits.

Bonus tip: Ask your lender if they offer appraisal waivers for certain loan types—this can save time and money.

Bonus Strategies to Accelerate Closing

Use a Mortgage Broker Like Level Mortgage

Mortgage brokers work with multiple lenders and can match you with one that offers faster underwriting and flexible terms. Level Mortgage specializes in quick closings and personalized service.

Consider Loan Recasting or Refinancing

If you’re refinancing, look into loan recasting—making a lump-sum payment to reduce monthly payments without changing your interest rate or term. It’s faster and less paperwork-intensive than full refinancing.

Opt for a Biweekly Payment Plan

While this doesn’t speed up closing, it helps pay off your mortgage faster post-closing. Making biweekly payments instead of monthly can shave 4–6 years off a 30-year mortgage.

The Bottom Line

Closing a mortgage loan faster is all about preparation, responsiveness, and working with the right professionals. By following these five tips and bonus strategies, you can reduce stress, save money, and move into your new home with confidence.

Want personalized assistance? Visit our 'Contact Us' tab and leave your information with one of our experts.

About Us

A group of like-minded seasoned veterans came together to create a company with an employee-focused culture. A culture that values its members both personally and professionally and a company built on the idea that the customer comes first!

We do not share data with third parties for marketing/promotional purposes.

By submitting your phone number to Level Mortgage, you are authorizing a representative of our company to send you text messages and notifications. Message frequency may vary. Message/data rates apply. Reply STOP to unsubscribe to a message sent from us, and HELP to receive help.

What to Know About Single Unit vs. Multifamily Investing

Florida’s real estate market continues to attract investors nationwide, but choosing between single-unit and multifamily properties requires a strategic understanding of mortgage financing, rental dynamics, and long-term wealth potential. This guide breaks down the key differences, benefits, and risks of each investment type—backed by 2025 data and mortgage loan insights.

Single-Unit vs. Multifamily: What’s the Difference?

– Single-unit properties refer to standalone homes, townhouses, or condos designed for one household.

– Multifamily properties include duplexes, triplexes, quadplexes, and apartment buildings with two or more rental units.

Both asset classes offer income potential, but they differ significantly in financing structure, scalability, and risk exposure.

Mortgage Loan Structures: Key Differences

1. Single-Unit Financing

Loan Type: Conventional, FHA, VA, and USDA loans are widely available.

Down Payment: Typically 3%–20% depending on loan type and credit profile.

Interest Rates: Slightly lower than multifamily loans due to reduced risk.

Florida’s population surged 8.5% between 2020 and 2024, driven by retirees, remote workers, and international migration. This growth fuels rental demand across both single and multifamily sectors.

Rental Rates:

Median Home Price (FL): $410,400

Investment Performance & Wealth Building

Multifamily Advantages

– Economies of Scale: One roof, multiple rents. A quadplex renting at $2,000/unit generates $8,000/month. With $5,500 debt service, DSCR = 1.45.

– Risk Diversification: Vacancy in one unit doesn’t eliminate income.

– Institutional Appeal: Easier to scale portfolios and attract capital.

Single-Unit Advantages

– Lower Entry Barriers: Easier for first-time investors.

– Appreciation Potential: Strong in suburban areas with limited inventory.

– Simpler Financing: More lenders, lower rates, and easier underwriting.

– Resale Flexibility: Easier to sell to owner-occupants.

DSCR Loans: A Game-Changer for Multifamily

DSCR (Debt Service Coverage Ratio) = Gross Rental Income ÷ Debt Obligations

– Most lenders require DSCR > 1.1 or 1.2.

– Example: Triplex renting at $1,800/unit = $5,400/month. Debt service = $4,000 → DSCR = 1.35.

– Benefits:

– No personal income verification.

– Ideal for self-employed investors.

– Strong cushion against vacancies.

Regional Investment Hotspots

North Florida (e.g., Jacksonville, Pensacola)

– Lower purchase prices.

– High rent-to-price ratios.

– Rent growth: 4%–6% annually.

Central Florida (e.g., Orlando)

– Balanced appreciation.

– Tourism-driven rental demand.

South Florida (e.g., Miami, Fort Lauderdale)

– High rents.

– Strong demand from international tenants.

Final Thoughts

Choosing between single-unit and multifamily investing in Florida depends on your financial goals, risk tolerance, and mortgage strategy. Single-family homes offer simplicity and appreciation, while multifamily properties deliver scalability and income stability—especially when paired with DSCR loans.

For investors seeking long-term cash flow and portfolio growth, multifamily assets in Florida’s thriving rental markets may offer the edge in 2025.

Want personalized assistance? Visit our 'Contact Us' tab and leave your information with one of our experts.

About Us

A group of like-minded seasoned veterans came together to create a company with an employee-focused culture. A culture that values its members both personally and professionally and a company built on the idea that the customer comes first!

We do not share data with third parties for marketing/promotional purposes.

By submitting your phone number to Level Mortgage, you are authorizing a representative of our company to send you text messages and notifications. Message frequency may vary. Message/data rates apply. Reply STOP to unsubscribe to a message sent from us, and HELP to receive help.

Top 10 Tax Benefits of Homeownership in Florida (2025 Guide)

Florida’s real estate market continues to shine in 2025—not just for its sun-soaked beaches and booming property values, but also for the compelling tax advantages it offers homeowners. Whether you’re a first-time buyer, seasoned investor, or relocating retiree, understanding the tax benefits of owning property in Florida can significantly impact your financial planning and long-term wealth strategy.

Why Florida? A Tax-Friendly Oasis

Florida ranks as the third most tax-friendly state in the U.S. in 2025. The absence of a state income tax is a major draw, especially for high-income earners, entrepreneurs, and retirees. This alone can save residents thousands of dollars annually compared to states like New York or California.

1. No State Income Tax

Florida’s constitution prohibits a state income tax, meaning:

– 100% of your salary, pension, or investment income stays with you

– Retirees benefit from no taxation on Social Security, pensions, or IRA withdrawals

– Remote workers and business owners relocating to Florida can see effective tax savings of 5–10% compared to income-taxed states

This foundational benefit sets the stage for additional tax perks tied directly to homeownership.

2. Homestead Exemption: Up to $50,000 in Taxable Value Reduction

Florida’s Homestead Exemption is one of the most powerful tools for reducing property taxes:

– Homeowners who declare their Florida property as their primary residence can receive up to $50,000 off their home’s assessed value

– The first $25,000 applies to all property taxes, including school district levies

– More residents qualify, including those with lower-value homes

– Tax savings can be transferred when moving to a new Florida home, preserving benefits

3. Save Our Homes Cap: Protection Against Rising Property Values

Florida’s Save Our Homes (SOH) provision limits the annual increase in assessed value of a homesteaded property to 3% or the rate of inflation, whichever is lower.

This is crucial in a market like Florida, where property values have risen by 6.8% year-over-year in 2025, according to Florida Realtors. Without SOH, property taxes could skyrocket. With it:

– Homeowners enjoy predictable and manageable tax bills

– Long-term residents save thousands over time as market values climb

4. Mortgage Interest Deduction

On the federal level, homeowners can deduct mortgage interest paid on loans up to $750,000 (for loans originated after December 15, 2017). This deduction is especially valuable in the early years of a mortgage, when interest payments are highest.

For example:

– A homeowner with a $500,000 mortgage at 6.5% interest pays roughly $32,500 in interest annually

– This amount can be deducted from taxable income, potentially saving $7,000–$9,000 depending on the tax bracket

5. Property Tax Deduction (Federal SALT Cap)

Homeowners can also deduct state and local property taxes on their federal return, subject to the $10,000 SALT cap (State and Local Tax).

– Most Florida homeowners stay well within the SALT cap

– A $400,000 home in Florida typically incurs $3,320 in annual property taxes, which can be fully deducted

6. Energy-Efficient Home Tax Credits

In 2025, federal tax credits for energy-efficient upgrades remain robust:

– Homeowners can claim up to 30% of the cost of eligible improvements, such as solar panels, heat pumps, and insulation

– Florida’s climate makes solar especially viable—solar installations increased by 22% statewide in 2025

These credits not only reduce tax liability but also lower utility bills, creating a double win.

7. Capital Gains Exclusion on Sale of Primary Residence

When selling a primary residence, homeowners may exclude up to:

– $250,000 of capital gains (single filers)

– $500,000 (married couples filing jointly)

To qualify, you must have:

– Owned and lived in the home for at least two of the last five years

– Not claimed the exclusion on another home in the past two years

With Florida’s property appreciation averaging 6–8% annually, many homeowners benefit from this exclusion when cashing out equity.

8. Home Equity Loan Interest Deduction

Interest on home equity loans or lines of credit (HELOCs) may be deductible if the funds are used to:

Buy, build, or substantially improve the home

This allows homeowners to tap into rising equity for renovations while enjoying tax benefits. In 2025, Florida’s average home equity has risen by 12.4%, making this strategy increasingly popular.

9. No Estate or Inheritance Tax

Florida does not levy estate or inheritance taxes, which is a major advantage for legacy planning:

– Heirs can inherit property without additional state-level taxation

– Combined with federal estate tax thresholds ($13.61 million in 2025), most estates pass tax-free

This makes Florida especially attractive for retirees and high-net-worth individuals.

10. Rental Income Opportunities and Tax Treatment

Florida’s thriving tourism and snowbird seasons create strong demand for short-term rentals:

– Rental income is taxable, but expenses like maintenance, utilities, and depreciation are deductible

– Many homeowners use platforms like Airbnb or VRBO to generate $20,000–$40,000 annually

In 2025, over 18% of Florida homeowners report earning supplemental income from rentals, according to the Florida Department of Revenue.

Final Thoughts: Strategic Ownership Pays Off

Homeownership in Florida offers more than lifestyle perks—it’s a strategic financial move. With no state income tax, generous exemptions, and federal deductions, homeowners can save thousands annually while building equity in a high-growth market.

To maximize these benefits:

– File for Homestead Exemption early in the year

– Keep records of mortgage interest and property tax payments

– Consult a tax professional when selling or renovating

– Explore energy-efficient upgrades for long-term savings

Want personalized assistance? Visit our 'Contact Us' tab and leave your information with one of our experts.

About Us

A group of like-minded seasoned veterans came together to create a company with an employee-focused culture. A culture that values its members both personally and professionally and a company built on the idea that the customer comes first!

We do not share data with third parties for marketing/promotional purposes.

By submitting your phone number to Level Mortgage, you are authorizing a representative of our company to send you text messages and notifications. Message frequency may vary. Message/data rates apply. Reply STOP to unsubscribe to a message sent from us, and HELP to receive help.

Renting vs. Buying a Home in Florida (2025): Which Is the Smarter Financial Move?

Florida’s real estate market has always been a magnet for both homeowners and renters. With its warm climate, no state income tax, and vibrant lifestyle, the question of whether to buy or rent in Florida is more relevant than ever in 2025. Let’s break down the numbers, trends, and key considerations to help you make an informed decision.

Florida’s 2025 Housing Market Snapshot

As of mid-2025, Florida’s housing market is showing signs of stabilization after the explosive growth of the early 2020s. According to Florida Realtors:

– Median Home Price (Single Family): $415,000 — down 2.7% from 2024

– Median Condo/Townhouse Price: $310,000 — down 6.1%

– Inventory Levels: 5.6 months for single-family homes (balanced market); 10.3 months for condos/townhouses (strong buyer’s market)

These figures suggest that while prices have cooled slightly, affordability remains a challenge due to elevated interest rates and insurance costs.

The Case for Buying

1. Building Equity

Homeownership allows you to build equity over time. With Florida’s long-term appreciation trends, buying can be a powerful wealth-building tool.

From 2015 to 2022, Florida home prices rose by over 80% in some counties.

Even with recent cooling, projections suggest median home prices could reach $470,000–$500,000 by 2030.

2. Tax Benefits

Florida homeowners enjoy:

No state income tax

Mortgage interest deductions (federal)

Homestead exemptions that reduce property tax bills

3. Stability and Control

Owning a home means:

No rent hikes

Freedom to renovate

Long-term stability, especially for families

4. Rental Income Potential

Florida’s tourism and snowbird seasons make short-term rentals lucrative. Platforms like Airbnb have made it easier for homeowners to monetize their properties.

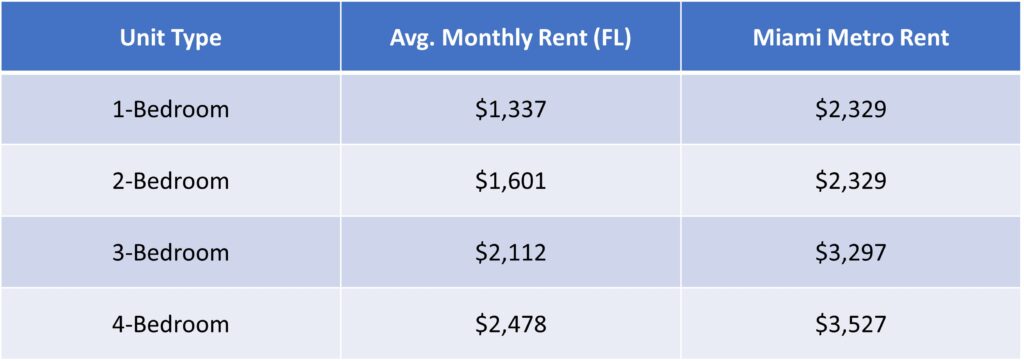

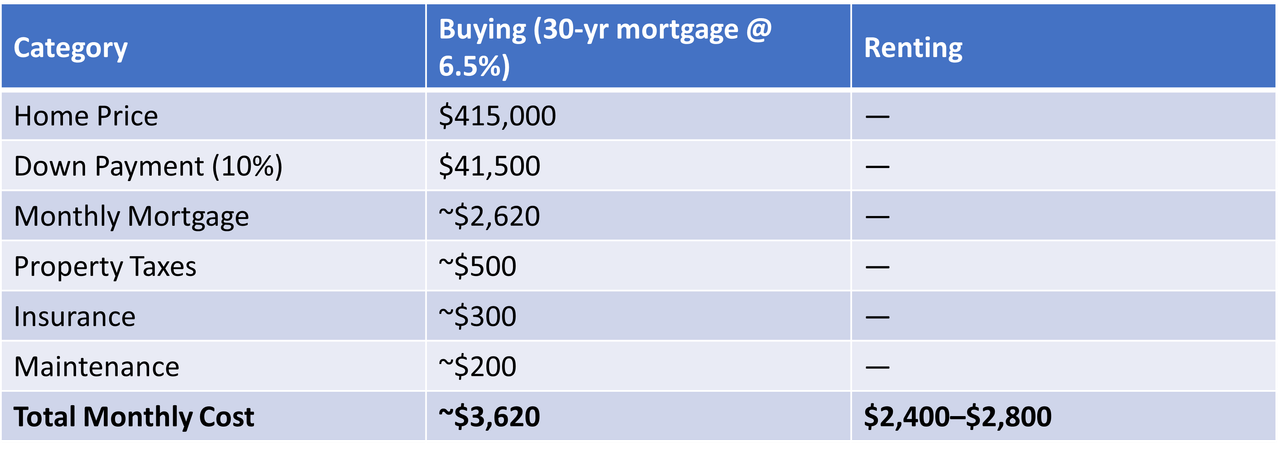

Cost Comparison: Renting vs. Buying in Florida (2025)

Let’s compare monthly costs for a typical single-family home:

Note: Rental prices vary by city. Miami and Naples tend to be higher, while Ocala and Lakeland are more affordable.

Regional Considerations

South Florida (Miami, Fort Lauderdale)

High property values and insurance costs

Strong rental demand

Buying may be viable for long-term residents or investors

Central Florida (Orlando, Tampa)

Balanced market conditions

Growing job market

Good mix of affordable rentals and homes

North Florida (Jacksonville, Tallahassee)

Lower home prices

Less volatility

Buying is more accessible for first-time buyers

What the Experts Say

Florida Realtors Chief Economist Dr. Brad O’Connor notes that “single-family homes ended 2024 still just barely in a seller’s market at 4.7 months of supply, while condos and townhouses are now firmly in buyer’s market territory, at 8.2 months’ supply”.

Meanwhile, Norada Real Estate predicts a “robust recovery” in home prices by 2030, driven by population growth and economic expansion.

Common Issues & FAQs

Can a buyer waive the mortgage contingency?

Yes, but it’s risky unless the buyer is paying all cash or has guaranteed financing.

Is an appraisal part of the mortgage contingency?

Yes. The lender must receive an appraisal satisfactory to them. If the appraisal is too low, the buyer may not get loan approval.

What happens if the buyer doesn’t notify the seller in time?

If the buyer fails to terminate the contract before the deadline, they may be obligated to proceed or forfeit their deposit.

Final Thoughts: Which Is Better?

The answer depends on your goals:

– Buy if you plan to stay for 5+ years, want to build equity, and can afford the upfront costs.

– Rent if you value flexibility, are unsure about your future, or want to avoid high insurance and maintenance costs.

In 2025, Florida’s market is more balanced than it’s been in years. That means buyers have more negotiating power, and renters have more options. Whether you’re eyeing a beachfront condo or a suburban bungalow, understanding the numbers is key.

Want personalized assistance? Visit our 'Contact Us' tab and leave your information with one of our experts.

About Us

A group of like-minded seasoned veterans came together to create a company with an employee-focused culture. A culture that values its members both personally and professionally and a company built on the idea that the customer comes first!

We do not share data with third parties for marketing/promotional purposes.

By submitting your phone number to Level Mortgage, you are authorizing a representative of our company to send you text messages and notifications. Message frequency may vary. Message/data rates apply. Reply STOP to unsubscribe to a message sent from us, and HELP to receive help.

Ave Maria’s 2025 New Home Sales Surge Mid-Year: A Testament to Resilience and Demand

Nestled in Eastern Collier County, Florida, Ave Maria continues to defy national housing market headwinds with a robust performance in new home sales through the first half of 2025. As a professional in the mortgage and real estate industry, it’s clear that Ave Maria’s success is not just a local anomaly—it’s a case study in strategic community planning, diversified housing options, and lifestyle-driven demand..

Mid-Year Sales Snapshot: 318 New Homes Sold

As of July 2025, Ave Maria recorded the sale of 318 new homes in the first six months of the year. This performance has earned the community the #18 spot on the prestigious RCLCO Top-Selling Master-Planned Communities in the U.S. list. Despite broader market challenges, including rising interest rates and inventory constraints, Ave Maria’s numbers reflect a healthy appetite for new construction in Southwest Florida.

Total Sales and Build-Out Vision

To date, Ave Maria has sold 5,500 new homes, with a projected total of 11,000 residences at full build-out. This milestone places the development halfway through its long-term vision, which includes not only residential expansion but also 1.8 million square feet of retail, office, and business park space across 5,000 acres.

Market Dynamics: Pricing and Inventory

According to Redfin and Realtor.com data:

– Median listing price: $468,000 (July 2025)

– Median sold price: $398,200

– Median price per square foot: $234

– Sale-to-list price ratio: 95.07%

– Average days on market: 78 days (up from 46 days in 2024)

While prices have dipped slightly—down 5.4% year-over-year—the community remains attractive to buyers seeking value, lifestyle, and long-term growth potential.

Builders Driving Growth

Ave Maria’s success is powered by four major residential builders:

– CC Homes

– Del Webb Naples

– Lennar

– Pulte Homes

These builders offer a wide range of housing options, including:

– Condominiums

– Attached villas

– Single-family homes

Prices range from the mid-$200,000s to the $800,000s, with over 25 designer-furnished model homes available for daily tours.

Why Buyers Choose Ave Maria

Michelle Mambuca, marketing and PR manager for the community, attributes the strong sales to Ave Maria’s “vibrant lifestyle, family-friendly amenities, conveniences, and variety of new home options”. Here’s what makes Ave Maria stand out:

Amenities Galore

– Water park

– Soccer and baseball fields

– Fitness center

– Amphitheater

– Dog park

– Walking paths

– Championship golf

– Bocce, pickleball, and tennis courts

– Town Center with 75+ businesses, including Publix and Mobil

Education Excellence

– Ave Maria Elementary School (opening August 2026, capacity: 900 students)

– Private schools from preschool through university

– Zoned for A-rated Collier County public schools

Retail and Employment

– 1.8 million sq. ft. of commercial space planned

– On-site retail and dining

– Local employment opportunities

Migration Trends: Who’s Moving In?

Between February and April 2025, migration data shows:

– 60% of buyers searched to stay within the Ave Maria metro area

– 40% looked to move out

– Top inbound metros: Miami (3,331 searches), Chicago (1,949), New York (1,138)

This influx from major urban centers suggests that Ave Maria is increasingly viewed as a refuge for buyers seeking affordability, space, and community.

Market Challenges and Resilience

Despite national trends showing cooling demand and longer time on market, Ave Maria’s performance is notable:

– Median sale price down 21.3% YoY to $380K

– Average days on market increased to 116 days

– Yet, home sales in June 2025 rose to 30, up from 23 in June 2024

This resilience is a testament to the community’s appeal and the strategic efforts of its developers and planners.

Recognition and Awards

Ave Maria’s accolades include:

– Top 20 Master-Planned Community in the U.S. (2015–2024)

– Community of the Year

– Top Selling Single-Family Home Community in Southwest Florida

– Blue Zones Certified Community

– Del Webb Naples named a Top 20 Place to Retire

Additionally, Ave Maria was named one of the Top 100 Places to Live by Ideal Living Magazine in 2025.

Outlook for the Second Half of 2025

With 318 homes sold mid-year and continued demand from out-of-state buyers, Ave Maria is poised to exceed 600 new home sales by year-end, matching or surpassing its 2024 performance. The upcoming opening of Ave Maria Elementary and continued commercial development will likely fuel further interest.

Final Thoughts

Ave Maria’s mid-year performance in 2025 is more than just a bright spot—it’s a blueprint for how master-planned communities can thrive in uncertain markets. With a balanced mix of affordability, amenities, and strategic growth, Ave Maria is not just selling homes—it’s selling a lifestyle.

For mortgage professionals, investors, and homebuyers alike, Ave Maria represents a compelling opportunity in Florida’s evolving real estate landscape.

Want personalized assistance? Visit our 'Contact Us' tab and leave your information with one of our experts.

About Us

A group of like-minded seasoned veterans came together to create a company with an employee-focused culture. A culture that values its members both personally and professionally and a company built on the idea that the customer comes first!

We do not share data with third parties for marketing/promotional purposes.

By submitting your phone number to Level Mortgage, you are authorizing a representative of our company to send you text messages and notifications. Message frequency may vary. Message/data rates apply. Reply STOP to unsubscribe to a message sent from us, and HELP to receive help.