What to Know About Single Unit vs. Multifamily Investing

Florida’s real estate market continues to attract investors nationwide, but choosing between single-unit and multifamily properties requires a strategic understanding of mortgage financing, rental dynamics, and long-term wealth potential. This guide breaks down the key differences, benefits, and risks of each investment type—backed by 2025 data and mortgage loan insights.

Single-Unit vs. Multifamily: What’s the Difference?

– Single-unit properties refer to standalone homes, townhouses, or condos designed for one household.

– Multifamily properties include duplexes, triplexes, quadplexes, and apartment buildings with two or more rental units.

Both asset classes offer income potential, but they differ significantly in financing structure, scalability, and risk exposure.

Mortgage Loan Structures: Key Differences

1. Single-Unit Financing

Loan Type: Conventional, FHA, VA, and USDA loans are widely available.

Down Payment: Typically 3%–20% depending on loan type and credit profile.

Interest Rates: Slightly lower than multifamily loans due to reduced risk.

Florida’s population surged 8.5% between 2020 and 2024, driven by retirees, remote workers, and international migration. This growth fuels rental demand across both single and multifamily sectors.

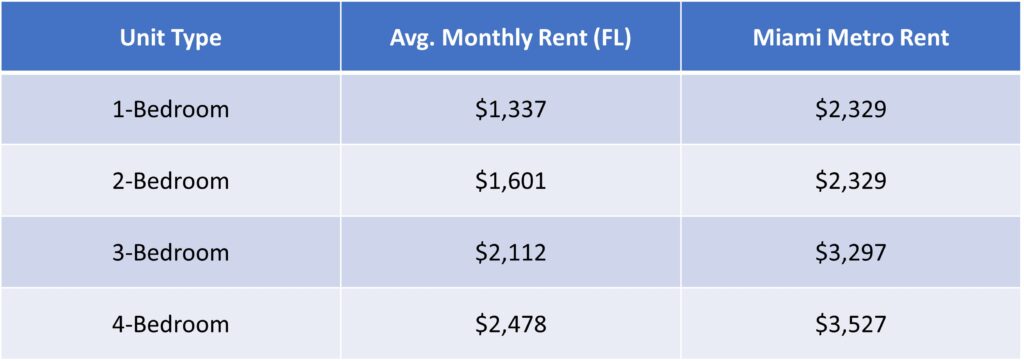

Rental Rates:

Median Home Price (FL): $410,400

Investment Performance & Wealth Building

Multifamily Advantages

– Economies of Scale: One roof, multiple rents. A quadplex renting at $2,000/unit generates $8,000/month. With $5,500 debt service, DSCR = 1.45.

– Risk Diversification: Vacancy in one unit doesn’t eliminate income.

– Institutional Appeal: Easier to scale portfolios and attract capital.

Single-Unit Advantages

– Lower Entry Barriers: Easier for first-time investors.

– Appreciation Potential: Strong in suburban areas with limited inventory.

– Simpler Financing: More lenders, lower rates, and easier underwriting.

– Resale Flexibility: Easier to sell to owner-occupants.

DSCR Loans: A Game-Changer for Multifamily

DSCR (Debt Service Coverage Ratio) = Gross Rental Income ÷ Debt Obligations

– Most lenders require DSCR > 1.1 or 1.2.

– Example: Triplex renting at $1,800/unit = $5,400/month. Debt service = $4,000 → DSCR = 1.35.

– Benefits:

– No personal income verification.

– Ideal for self-employed investors.

– Strong cushion against vacancies.

Regional Investment Hotspots

North Florida (e.g., Jacksonville, Pensacola)

– Lower purchase prices.

– High rent-to-price ratios.

– Rent growth: 4%–6% annually.

Central Florida (e.g., Orlando)

– Balanced appreciation.

– Tourism-driven rental demand.

South Florida (e.g., Miami, Fort Lauderdale)

– High rents.

– Strong demand from international tenants.

Final Thoughts

Choosing between single-unit and multifamily investing in Florida depends on your financial goals, risk tolerance, and mortgage strategy. Single-family homes offer simplicity and appreciation, while multifamily properties deliver scalability and income stability—especially when paired with DSCR loans.

For investors seeking long-term cash flow and portfolio growth, multifamily assets in Florida’s thriving rental markets may offer the edge in 2025.

Want personalized assistance? Visit our 'Contact Us' tab and leave your information with one of our experts.

About Us

A group of like-minded seasoned veterans came together to create a company with an employee-focused culture. A culture that values its members both personally and professionally and a company built on the idea that the customer comes first!

We do not share data with third parties for marketing/promotional purposes.

By submitting your phone number to Level Mortgage, you are authorizing a representative of our company to send you text messages and notifications. Message frequency may vary. Message/data rates apply. Reply STOP to unsubscribe to a message sent from us, and HELP to receive help.