How to Finance a New Construction Condo Before Completion

the National Association of Realtors (NAR), the supply of existing homes remains well below the levels needed to satisfy buyer demand. This scarcity has pushed investors and primary residents alike toward a compelling alternative: pre-construction condos.

In high-growth hubs like Miami, Fort Lauderdale, and West Palm Beach, the skyline is a constant rotation of cranes. For many, buying “off-plan”—purchasing a unit before the building is even finished—is the only way to secure a prime piece of real estate in a competitive market. However, financing a property that doesn’t technically exist yet is a vastly different beast than a traditional resale purchase.

Understanding the mechanics of developer deposits, mortgage timing, and capital leverage is essential for any buyer looking to capitalize on the new construction boom.

Why Buyers Choose Pre-Construction Condos

The primary draw of pre-construction is the “early bird” advantage. Unlike the resale market, where you are competing with multiple offers on an aging asset, pre-construction allows you to lock in a price based on today’s market values for a product that won’t be delivered for two to four years.

1. Built-In Appreciation

In a healthy real estate market, a condo often appreciates significantly during its construction phase. Industry data suggests that pre-construction units in Tier-1 cities like Miami can see a 10% to 25% increase in value between the time the contract is signed and the day the keys are handed over. Essentially, you are “buying” the future equity.

2. Customization and Modern Incentives

Developers often offer incentives to early-stage buyers, including the ability to select finishes, floorings, and appliances. Furthermore, new buildings are constructed to the latest Florida Building Codes, which significantly reduces long-term maintenance costs and insurance premiums—a major factor in today’s high-cost insurance environment.

3. Favorable Entry Pricing

During the “friends and family” or “first tier” of sales, developers frequently price units lower to hit the sales quotas required to trigger their construction financing.

The Most Common Ways to Finance a Pre-Construction Condo

Because a bank cannot place a lien on a property that isn’t finished, you cannot get a standard mortgage on day one. Instead, financing a pre-construction condo is a two-phase process: the Deposit Phase and the Closing Phase.

Developer Deposit Structure

In most U.S. markets, and specifically in Florida, developers follow a “staggered” deposit schedule. Instead of a 20% down payment at the start, you pay in installments. A typical structure looks like this:

10% at Reservation: Held in escrow while you review the offering plan.

10% at Contract Execution: Totaling 20% down to secure the unit.

10% at Groundbreaking: When the foundation work begins.

10% at “Top-Off”: Once the building reaches its highest structural point.

Remaining 60% (Balance) at Closing: Typically covered by a traditional mortgage.

Developers require these deposits to secure their own construction loans and ensure buyer commitment.

Traditional Mortgage at Closing

The actual “financing” through a lender typically happens only when the building receives its Certificate of Occupancy (CO).

The Pre-Approval: You should be pre-approved at the time of contract to ensure you can afford the unit.

The Final Loan: You will apply for the formal mortgage 60 to 90 days before the building is finished.

Lender Requirements: The lender will evaluate the building’s health, ensuring at least 50% of units are under contract and the condo association has adequate reserves (often 10% of the total budget).

Using a HELOC or Home Equity Loan

Many savvy investors do not use their “cash on hand” for the initial deposit phase. Instead, they leverage the equity in their current primary residence or other investment properties.

Strategy: By opening a Home Equity Line of Credit (HELOC), an investor can draw the 10% increments needed for the developer deposits.

Benefit: This allows the investor to keep their liquid cash working in other investments while using a lower-interest credit line to secure the new condo.

Private or Portfolio Lenders

If a building is “non-warrantable” (meaning it doesn’t meet Fannie Mae or Freddie Mac standards, often due to high investor concentration), traditional banks might shy away. In these cases, portfolio lenders or private lenders step in. These entities keep the loans on their own books, allowing for more flexible debt-to-income (DTI) requirements and lending to foreign nationals—a massive demographic in the Miami luxury condo market.

Key Financial Requirements Buyers Should Prepare

Lenders treat new construction condos with a higher level of scrutiny. To ensure your financing goes smoothly at the finish line, you should aim for the following benchmarks:

Credit Score: While FHA loans allow lower scores, most condo lenders prefer a 720 or higher to secure the best interest rates.

Debt-to-Income (DTI) Ratio: Lenders generally want your total monthly debt payments (including the new mortgage, HOA fees, and taxes) to be under 43% of your gross monthly income.

Liquid Reserves: Be prepared to show 6 to 12 months of “PITI” (Principal, Interest, Taxes, and Insurance) in a liquid account after the down payment is made.

Appraisal: The property must appraise for the purchase price at the time of completion. If the market dips and the appraisal comes in low, the buyer is responsible for covering the gap in cash.

Risks Buyers Should Understand Before Financing

While the rewards are high, pre-construction carries unique risks that aren’t present in the resale market.

Interest Rate Volatility: You sign a contract today, but you won’t get a mortgage for two years. If interest rates rise from 6% to 8% in that time, your monthly payment could increase significantly.

Construction Delays: According to the U.S. Census Bureau, large-scale residential projects can face delays of 6 to 12 months due to labor shortages or supply chain issues. You must ensure your financial situation is stable enough to wait.

Market Fluctuations: While appreciation is expected, it is not guaranteed. If the market oversupplies units in a specific neighborhood, value growth may stagnate.

Why Pre-Construction Financing Can Be a Powerful Investment Strategy

Despite the risks, the data favors the long-term investor. Florida’s population grew by over 365,000 people between 2023 and 2024, maintaining its status as one of the fastest-growing states. This influx of residents creates a “floor” for demand.

By financing a pre-construction unit, you are essentially “locking in” a price in a high-inflation environment. If the cost of raw materials (lumber, steel, concrete) continues to rise, the replacement cost of the building goes up, naturally lifting the value of your unit before you’ve even moved in.

How Level Mortgage Can Help Buyers Finance New Construction Condos

Navigating the gap between a developer contract and a bank closing requires a sophisticated mortgage partner. At Level Mortgage, we specialize in bridge strategies and long-term financing for pre-construction buyers.

Pre-Approval for Future Deliveries: We help you understand your borrowing power years in advance.

Investor-Specific Products: Including DSCR (Debt Service Coverage Ratio) loans that focus on the property’s future rental income rather than your personal income.

HELOC Coordination: We can help you tap into existing equity to cover those initial developer deposits.

Guidance on “Non-Warrantable” Buildings: We have access to a wide network of portfolio lenders who specialize in luxury condo projects that traditional banks may avoid.

Final Thoughts

Financing a new construction condo is a marathon, not a sprint. Success depends on understanding the developer’s deposit timeline, maintaining a strong financial profile during the construction years, and choosing a lender who understands the nuances of the Florida market.

With the right strategy, buying pre-construction isn’t just a way to get a home—it’s a powerful vehicle for wealth creation.

Want personalized assistance? Visit our 'Contact Us' tab and leave your information with one of our experts.

About Us

A group of like-minded seasoned veterans came together to create a company with an employee-focused culture. A culture that values its members both personally and professionally and a company built on the idea that the customer comes first!

We do not share data with third parties for marketing/promotional purposes.

By submitting your phone number to Level Mortgage, you are authorizing a representative of our company to send you text messages and notifications. Message frequency may vary. Message/data rates apply. Reply STOP to unsubscribe to a message sent from us, and HELP to receive help.

Using a HELOC to Buy a Second Home: Pros, Cons & Mortgage Insights

For many homeowners in 2026, the greatest financial asset isn’t sitting in a savings account—it’s locked within the walls of their primary residence. As home values have maintained a steady upward trajectory over the last several years, tappable equity has reached record highs. If you are looking to expand your real estate portfolio or secure a vacation getaway, using a HELOC to buy a second home has emerged as a premier strategy for savvy investors and families alike.

Leveraging equity allows you to bypass the hurdles of liquidating cash reserves or selling off stocks in a volatile market. However, navigating the mortgage landscape in 2026 requires a nuanced understanding of interest rate trends and debt-to-income ratios. This guide explores how a Home Equity Line of Credit (HELOC) works and whether it is the right engine to power your next property purchase.

What Is a HELOC and How It Works

Despite regulatory shifts in some cities, the short‑term rental market remains strong. According to AirDNA’s 2025 U.S. Short‑Term Rental Outlook, national STR demand grew 7.8% year‑over‑year, and average daily rates increased 3.2% heading into 2026. Investor interest remains high because:

STRs often generate 20–40% higher gross rental income than comparable long‑term rentals in the same market.

Remote work and flexible travel trends continue to support year‑round occupancy.

Many secondary and tertiary markets have seen rising tourism and fewer regulatory restrictions.

However, higher potential returns also come with more complex financing requirements.

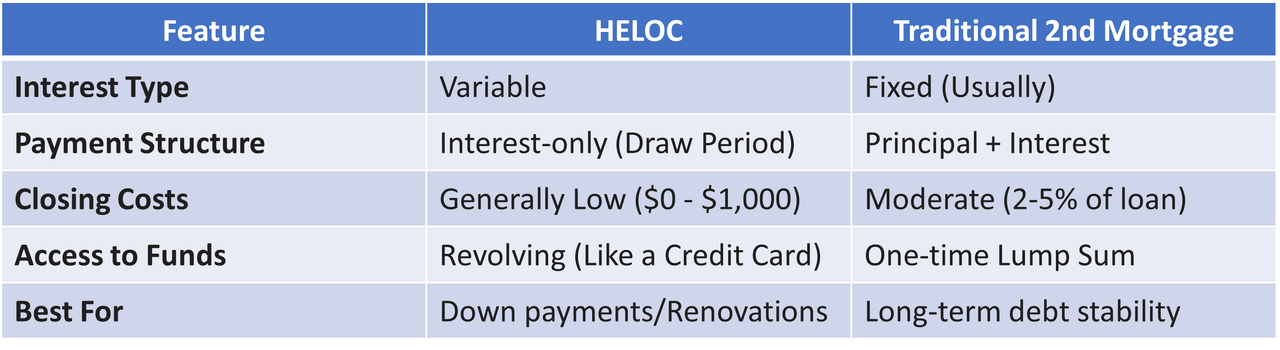

HELOC Basics

Loan Against Home Equity: Your credit limit is based on the appraised value of your home minus what you still owe on your primary mortgage.

Line of Credit vs. Lump Sum: You have the freedom to spend only what you need for a down payment or closing costs, leaving the rest of the credit line available for emergencies or renovations.

Interest-Only Draw Period: Most HELOCs offer a 10-year “draw period.” During this time, you typically only have to pay interest on the amount you’ve borrowed, which keeps initial monthly costs low while you manage a new second home.

Why Buyers Consider a HELOC for a Second Home Purchase

With the 2026 market showing signs of increased competition in the “second home” sector—driven by the continued normalization of remote work—buyers need to move fast. A HELOC provides “ready-to-go” capital that acts like cash in the eyes of a seller.

Financial Leverage & Timing

Using a HELOC allows you to maintain your liquidity. Instead of selling off stocks or dipping into a high-yield savings account (which may be earning 4-5% in today’s environment), you leverage the “dead equity” in your home. This strategy is particularly effective when you need to act quickly on a property listing before other buyers can secure traditional financing. It also allows you to bypass the need for a “home sale contingency” if you were planning to sell a different asset to fund the purchase.

Pros of Using a HELOC to Buy a Second Home

Leveraging your primary residence comes with distinct advantages that traditional second-home mortgages often lack:

Minimal Upfront Costs: HELOCs often have little to no closing costs. Many lenders in 2026 offer “no-cost” setups where they cover the appraisal and origination fees.

Borrow up to 85% CLTV: Most lenders allow a Combined Loan-to-Value (CLTV) of 80% to 85%. If your home is worth $1,000,000 and you owe $500,000, you could potentially access up to $350,000 in credit.

Tax Advantages: Per current IRS guidelines, the interest on a HELOC may be tax-deductible if the funds are used specifically to “buy, build, or substantially improve” the home that secures the loan.

Flexibility: You only pay interest on what you use. If you only need $50,000 for a down payment on a $250,000 condo, you aren’t forced to pay interest on a full $250,000 loan.

Cons & Risks of Using a HELOC for a Second Home

Despite the benefits, this strategy is not without significant risk. In the 2026 economy, borrowers must be wary of “rate creep” and equity volatility.

Variable Interest Rates: HELOCs are almost always tied to the Prime Rate. If the Federal Reserve raises rates to combat inflation, your HELOC payment will climb immediately.

Collateral Risk: Your primary home is the collateral. If you experience a financial hardship and cannot pay the HELOC, you risk losing the roof over your head.

Future Payment Shock: Once the 10-year draw period ends, the loan enters the “repayment period” (usually 20 years). At this point, you must pay both principal and interest, which can cause your monthly payment to double or even triple.

Rate Volatility & Market Conditions

Over the last 5 to 10 years, we have seen the Prime Rate move from near-zero to over 8%. While 2026 forecasts suggest a period of relative stability, a 2% increase in the Prime Rate can add significant stress to a household budget that is already managing two properties. Borrowers should always calculate their “break-even” point—the highest interest rate they could afford before the second home becomes a financial burden.

How Lenders Evaluate HELOC Usage

Securing a HELOC in 2026 is a more rigorous process than it was a decade ago. Lenders are looking for “pristine” borrowers who can weather economic shifts.

Credit Score: A FICO score of 720+ is typically required for the best rates, though some lenders will go down to 680 with higher interest margins.

Debt-to-Income (DTI): Most lenders want to see a DTI of 43% or lower. This calculation includes your primary mortgage, the new HELOC payment, and the projected costs of the second home (taxes, insurance, and HOA).

Home Equity: You usually need at least 15-20% equity remaining in the home after the HELOC is taken out.

Occupancy Type: Lenders will ask if the second home is a “vacation home” or an “investment property.” Investment properties often carry stricter requirements and slightly higher rates.

Smart Strategies for Using a HELOC to Buy Your Second Home

The Down Payment Bridge: Use the HELOC only for the 20% down payment. This allows you to avoid Private Mortgage Insurance (PMI) on your second home mortgage while keeping your cash reserves intact.

The “Fix and Refi”: Use the HELOC to buy a property that needs work. Once the renovations are complete and the value of the second home has increased, perform a “cash-out refinance” on the second home to pay off the HELOC on your primary home.

Aggressive Principal Reduction: During the 10-year draw period, don’t just pay the interest. Treat it like a fixed loan and pay down the principal monthly to reduce your long-term interest exposure.

HELOC vs. Traditional Second Mortgage

Real-World Example (Hypothetical)

magine a homeowner in 2026 with the following profile:

Primary Residence Value: $800,000

Current Mortgage: $400,000

Available Equity: $400,000

They find a beach cottage for $500,000. Instead of taking out a full $500,000 mortgage at 6.5%, they use their HELOC to pull $100,000 (20%) for a down payment. They then finance the remaining $400,000 with a traditional mortgage.

By using the HELOC, they avoided a “Jumbo” loan category (if applicable) and kept $100,000 in their brokerage account, which is currently yielding 8% annually. The “cost of capital” from the HELOC is offset by the “return on capital” from their investments.

What This Means for Buyers & Investors in 2026

The 2026 market is characterized by steady, if not explosive, growth. Rental demand remains high as many would-be buyers stay on the sidelines due to inventory shortages. For the savvy investor, using a HELOC to buy a second home is a way to capitalize on this rental demand.

However, keep an eye on the Tax Cuts and Jobs Act (TCJA) provisions, as tax laws regarding interest deductibility can shift. In 2026, the strategy is about precision: using just enough equity to secure the deal without over-leveraging your foundation.

Conclusion: Is a HELOC Right for You?

Leveraging your home equity to expand your real estate holdings is one of the fastest ways to build long-term wealth. A HELOC provides the speed and flexibility needed in a modern market, but it requires a disciplined repayment strategy and a keen eye on interest rate trends.

Before you tap into your equity, it is essential to have a professional evaluate your debt-to-income ratio and your long-term goals.

Would you like a personalized equity analysis to see how much you can borrow? Contact Level Mortgage today to explore HELOC options tailored to your second home goals.

Want personalized assistance? Visit our 'Contact Us' tab and leave your information with one of our experts.

About Us

A group of like-minded seasoned veterans came together to create a company with an employee-focused culture. A culture that values its members both personally and professionally and a company built on the idea that the customer comes first!

We do not share data with third parties for marketing/promotional purposes.

By submitting your phone number to Level Mortgage, you are authorizing a representative of our company to send you text messages and notifications. Message frequency may vary. Message/data rates apply. Reply STOP to unsubscribe to a message sent from us, and HELP to receive help.

Buying a home in Florida is an exciting milestone, especially for first-time buyers. However, the mortgage application process can feel overwhelming if you’re not prepared. Understanding the do’s and don’ts of applying for a mortgage can save you time, money, and stress—and help you secure the best possible loan terms.

The Do’s of Applying for a Mortgage

Do Check Your Credit Early

Lenders rely heavily on your credit score to determine eligibility and interest rates.

According to Fannie Mae, borrowers with higher credit scores often qualify for lower rates, potentially saving thousands over the life of the loan.

In Florida, where median home prices reached $405,000 in late 2025 (NAR data), even a 0.5% difference in interest rate can significantly impact affordability.

Do Get Pre-Approved

Pre-approval shows sellers you’re a serious buyer and gives you a clear budget.

New credit inquiries can lower your score and raise red flags.

Lenders may see new debt as a risk, especially during underwriting.

Don’t Make Large, Unverified Deposits

Any unexplained deposit can trigger questions about the source of funds.

Always document gifts or transfers with proper paperwork.

Don’t Change Jobs Without Consulting Your Lender

Even a promotion can complicate income verification.

Stability is key—wait until after closing to make career moves.

Don’t Ignore Your Debt-to-Income Ratio (DTI)

Most lenders prefer a DTI below 43%, though FHA may allow slightly higher.

Adding new debt (like financing a car) during the process can push you over the limit.

Don’t Skip Professional Guidance

Mortgage brokers and loan officers can help you compare options.

According to Fannie Mae’s 2024 survey, 71% of buyers said digital mortgage tools made the process easier, but expert guidance remains invaluable.

Florida Market Insights

Florida’s housing market remains competitive, with strong demand in coastal cities and suburban areas.

Rising interest rates in 2025–2026 have cooled some buyer activity, but affordability programs continue to support first-time buyers.

The Federal Reserve noted that mortgage rates averaged 6.7% in late 2025, up from historic lows in 2021. This makes preparation and smart financial moves more critical than ever.

Actionable Tips for Florida Homebuyers

Start early: Check credit and savings at least six months before applying.

Stay consistent: Avoid financial changes until after closing.

Leverage programs: Explore FHA, VA, USDA, and Florida-specific assistance.

Work with experts: Partner with trusted mortgage professionals like Level Mortgage to navigate the process.

Think long-term: Choose a loan that fits both your current budget and future goals.

Conclusion

Applying for a mortgage in Florida doesn’t have to be stressful. By following the do’s—like maintaining stable income, getting pre-approved, and exploring assistance programs—and avoiding the don’ts—like opening new credit or making undocumented deposits—you’ll position yourself for success. With preparation and guidance, you can secure financing confidently and move closer to owning your Florida dream home.

Want personalized assistance? Visit our 'Contact Us' tab and leave your information with one of our experts.

About Us

A group of like-minded seasoned veterans came together to create a company with an employee-focused culture. A culture that values its members both personally and professionally and a company built on the idea that the customer comes first!

We do not share data with third parties for marketing/promotional purposes.

By submitting your phone number to Level Mortgage, you are authorizing a representative of our company to send you text messages and notifications. Message frequency may vary. Message/data rates apply. Reply STOP to unsubscribe to a message sent from us, and HELP to receive help.

Why Waiting for the “Perfect Rate” to Refinance Might Cost You More

The Florida Mortgage Landscape in 2026

Mortgage rates in Florida—and nationwide—have cooled from their 2023 highs but remain in the 6.0–6.2% range for 30-year fixed loans. Freddie Mac reports the average 30-year fixed mortgage at 6.10% as of January 2026, while Fannie Mae forecasts rates to hover near 6.0% through mid-2026.

For Florida homeowners, this means refinancing opportunities are available now. But many hesitate, waiting for the “perfect” rate—often a psychological anchor like 5% or lower. The reality? That wait can cost more than it saves.

The Myth of the “Perfect Rate”

Rate Anchoring Bias

Homeowners often anchor to past rates (like the 3% era of 2020–2021). This creates unrealistic expectations. Rates today are shaped by inflation, Federal Reserve policy, and housing demand—not nostalgia.

Market Timing Fallacy

Trying to predict the exact bottom of mortgage rates is like timing the stock market. Even experts at the Mortgage Bankers Association (MBA) caution that rates fluctuate weekly, and waiting often results in missed savings opportunities.

Why Waiting Can Cost You More

1. Opportunity Cost of Monthly Savings

Suppose you have a $300,000 mortgage at 7.25% (a common rate in 2023). Refinancing today at 6.1% saves about $210 per month.

Annual savings: $2,520

5-year savings: $12,600

Waiting for rates to drop to 5.5% might save an extra $100 per month—but if rates never reach that level, you’ve lost years of savings.

2. Long-Term Equity Impact

Lower monthly payments free up cash flow, allowing homeowners to build equity faster or invest elsewhere. Delaying refinancing means slower equity growth and less financial flexibility.

3. Florida-Specific Risks

Florida’s housing market remains competitive, with home prices up 6% year-over-year in 2025 according to MBA data. Rising property values mean waiting could also increase your loan-to-value ratio, potentially limiting refinance options or raising costs.

Real Numbers: Comparing Scenarios

Key takeaway: Waiting for 5.5% could save $8,100 over 5 years—but if rates stay at 6.1%, you lose $12,600 by not refinancing now.

Common Refinance Myths Debunked

Myth 1: “Rates will always go lower.”

Reality: Rates are influenced by inflation and Fed policy. The Federal Reserve has signaled cautious cuts, not dramatic drops.

Myth 2: “It’s better to wait until I hit the bottom.”

Reality: No one can consistently predict the bottom. Even professional forecasts vary within a 0.5% range.

Myth 3: “Refinancing isn’t worth it unless I save 1%.”

Reality: The CFPB notes that even a 0.5% reduction can yield significant long-term savings, especially on larger loans.

Psychological Traps to Avoid

Anchoring: Comparing today’s rates to pandemic-era lows.

Loss Aversion: Fear of missing out on a lower rate keeps borrowers stuck.

Overconfidence: Believing you can outsmart the market.

Recognizing these biases helps homeowners make rational, financially sound decisions.

Why Acting Now Makes Sense in Florida

Rates are stable around 6.0–6.2%, offering predictable refinance opportunities.

Home values are rising, meaning equity gains can be locked in sooner.

Demand is strong—refinance applications surged 40% in January 2026.

Florida homeowners who act now can secure savings and avoid the uncertainty of waiting.

The Advisor’s Perspective

As a trusted mortgage advisor with Level Mortgage, I’ve seen countless clients wait for the “perfect” rate—only to regret missing years of savings. The smarter move is to evaluate your refinance options today, based on your financial goals, not market speculation.

Conclusion

Refinancing in Florida at current rates can deliver immediate monthly savings, long-term equity growth, and financial flexibility. Waiting for the “perfect” rate is a gamble that often costs more than it saves.

Want personalized assistance? Visit our 'Contact Us' tab and leave your information with one of our experts.

About Us

A group of like-minded seasoned veterans came together to create a company with an employee-focused culture. A culture that values its members both personally and professionally and a company built on the idea that the customer comes first!

We do not share data with third parties for marketing/promotional purposes.

By submitting your phone number to Level Mortgage, you are authorizing a representative of our company to send you text messages and notifications. Message frequency may vary. Message/data rates apply. Reply STOP to unsubscribe to a message sent from us, and HELP to receive help.

What Happens After You’re Pre-Approved for a Mortgage

Getting pre-approved for a mortgage is a major milestone in the home-buying journey. In Florida’s dynamic real estate market, where single-family homes ended 2024 with 4.7 months of supply and condos shifted into a buyer’s market with 8.2 months of supply, pre-approval gives you a competitive edge.

But what happens next? Let’s break down the process step by step.

Mortgage balances account for $13.07 trillion, while HELOC balances rose by $11 billion, marking the 14th consecutive quarterly increase.

Credit card debt is surging, with balances exceeding $1.3 trillion nationwide, driven by inflation and consumer spending.

In Florida, where housing values have risen sharply post-pandemic, homeowners often have significant equity available. This makes HELOCs an attractive option for debt consolidation.

Step 3: Underwriting

The underwriting process verifies your financial documents, employment, and credit history.

Underwriting usually takes 1–2 weeks, depending on complexity.

Step 4: Closing Timeline

Most conventional loans in Florida close in 30–45 days from application to funding.

Closing involves signing final documents, transferring funds, and recording the deed.

Buyers should budget for closing costs between 2–5% of the loan amount.

Florida Market Context (2025)

Average mortgage rate in 2025: 6.25%

Buyer vs. Seller Market:

Single-family homes: 4.7 months of supply (seller’s market)

Condos/townhouses: 8.2 months of supply (buyer’s market)

These dynamics affect negotiation power after pre-approval.

Common Challenges After Pre-Approval

Job changes or new debt can jeopardize approval.

Low appraisals may require renegotiation.

Market competition in Florida means homes often receive multiple offers within days.

Tips for Buyers After Pre-Approval

Avoid major financial changes (new credit cards, car loans).

Respond quickly to lender requests for documentation.

Stay within your pre-approved budget to avoid delays.

Work closely with your real estate agent to navigate Florida’s shifting market conditions.

Conclusion

Pre-approval is just the beginning. From house hunting to closing, the process involves multiple steps—each critical to securing your home. In Florida’s 2025 market, where rates hover around 6.25% and supply varies by property type, being prepared after pre-approval can make the difference between closing smoothly or facing delays.

Want personalized assistance? Visit our 'Contact Us' tab and leave your information with one of our experts.

About Us

A group of like-minded seasoned veterans came together to create a company with an employee-focused culture. A culture that values its members both personally and professionally and a company built on the idea that the customer comes first!

We do not share data with third parties for marketing/promotional purposes.

By submitting your phone number to Level Mortgage, you are authorizing a representative of our company to send you text messages and notifications. Message frequency may vary. Message/data rates apply. Reply STOP to unsubscribe to a message sent from us, and HELP to receive help.

How to Prepare for Your First Consultation with a Mortgage Professional

Preparing for your first mortgage consultation is one of the most important steps in the homebuying process. Whether you’re purchasing your first home, relocating to Florida, or upgrading your current property, arriving prepared can dramatically improve your loan options, speed up approval, and help you understand your true buying power. According to industry guidance, the first consultation is designed to help you understand your options—not to obligate you to a loan application.

This guide breaks down everything you need to bring, what to expect, and how to position yourself for success in Florida’s competitive real estate market.

Why Your First Mortgage Consultation Matters

Your initial meeting with a mortgage professional sets the tone for your entire homebuying journey. It helps you:

Understand your loan options

Determine your purchasing power

Identify potential credit or financial issues early

Build a strategy for navigating Florida’s fast‑moving housing market

Mortgage experts emphasize that preparing ahead of time leads to a smoother experience from start to finish.

1. Know Your Homeownership Goals

Before your consultation, define what you want to accomplish. This helps the mortgage professional tailor recommendations.

Questions to Ask Yourself

Are you a first‑time buyer or repeat buyer?

Are you upsizing, downsizing, or relocating?

What Florida cities or counties are you targeting?

What is your ideal monthly payment?

How long do you plan to stay in the home?

Florida’s market is diverse—Miami, Tampa, Orlando, and Jacksonville each have different price points and lending dynamics. Knowing your goals helps your lender match you with the right loan program.

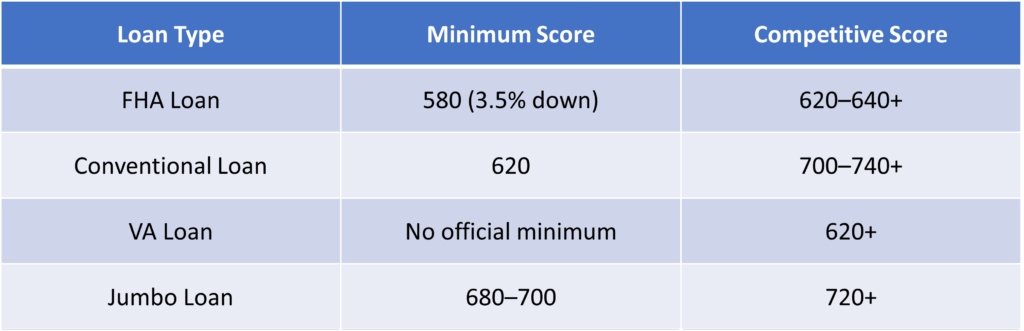

The average U.S. credit score is around 715 (FICO).

FHA loans allow scores as low as 580, but with higher costs.

Conventional loans typically require 620+.

If your score is lower than expected, your mortgage professional can help you create a plan to improve it before applying.

4. Understand Your Debt‑to‑Income Ratio (DTI)

DTI is a key metric lenders use to determine affordability.

Typical DTI Requirements

Conventional loans: up to 45%

FHA loans: up to 57% with strong compensating factors

VA loans: flexible but typically under 41%

Reducing debt before your consultation can significantly improve your loan options.

5. Research Florida Market Conditions

Florida’s real estate market remains one of the most active in the U.S. Understanding local trends helps you prepare realistic expectations.

Key Florida Market Facts (2025–2026)

Florida remains a top‑3 state for population growth.

Median home prices increased between 3%–6% in major metros year‑over‑year.

Inventory remains tight in coastal counties, increasing competition.

Your mortgage professional will help you understand how these trends affect your buying power.

6. Prepare Questions for Your Mortgage Professional

A consultation is a two‑way conversation. Bring questions that help you understand your options.

Smart Questions to Ask

What loan programs do I qualify for?

What down payment options are available?

What interest rate range should I expect?

What are the estimated closing costs?

How long does the approval process take?

Are there Florida‑specific programs I can use (Hometown Heroes, first‑time buyer grants, etc.)?

7. Understand What Happens During the Consultation

According to mortgage industry guidance, your consultation will typically include:

A review of your financial documents

A discussion of your goals and timeline

A preliminary assessment of your loan eligibility

An explanation of loan types (FHA, VA, USDA, Conventional, Jumbo)

A breakdown of estimated payments and costs

This meeting is designed to empower you with information—not pressure you into a loan.

8. Avoid Common Mistakes Before Your Consultation

Do NOT:

Make large purchases

Open new credit accounts

Transfer large sums between accounts

Change jobs without discussing it with your lender

These actions can negatively impact your loan eligibility.

9. Prepare for a Competitive Florida Market

Florida’s housing market is fast‑paced. Being prepared gives you an advantage.

Competitive Advantages You Gain by Preparing

Faster pre‑approval

Stronger offers

Better negotiation power

Ability to lock rates quickly

In markets like Miami‑Dade, Hillsborough, and Orange County, homes often receive multiple offers within days.

10. Final Checklist Before Your Consultation

Bring:

Financial documents

Credit report

List of questions

Notes about your goals

Proof of funds for down payment

Be Ready To Discuss:

Budget

Employment history

Savings

Timeline

Preferred loan type

Conclusion

Preparing for your first consultation with a mortgage professional is one of the smartest steps you can take as a Florida homebuyer. With the right documents, clear goals, and an understanding of your financial picture, you’ll walk into your meeting confident and ready to take the next step toward homeownership.

Want personalized assistance? Visit our 'Contact Us' tab and leave your information with one of our experts.

About Us

A group of like-minded seasoned veterans came together to create a company with an employee-focused culture. A culture that values its members both personally and professionally and a company built on the idea that the customer comes first!

We do not share data with third parties for marketing/promotional purposes.

By submitting your phone number to Level Mortgage, you are authorizing a representative of our company to send you text messages and notifications. Message frequency may vary. Message/data rates apply. Reply STOP to unsubscribe to a message sent from us, and HELP to receive help.

How Long Does It Take to Build Good Credit for a Mortgage?

Building good credit for a mortgage is one of the most important steps toward homeownership—especially in competitive markets like Florida, where strong credit can mean lower interest rates, smoother approvals, and thousands saved over the life of a loan. But how long does it actually take to build or rebuild credit to a “mortgage‑ready” level?

Below is a complete, Florida‑focused guide with timelines, statistics, and actionable steps.

Understanding What “Good Credit” Means for a Mortgage

Mortgage lenders rely heavily on your FICO® Score, which ranges from 300 to 850. While requirements vary by loan program, here are typical benchmarks:

In Florida’s fast‑moving real estate market—especially in areas like Tampa, Orlando, Miami, and Jacksonville—buyers with 700+ scores often secure the best rates and fastest approvals.

Factors That Influence How Fast You Can Build Credit

Your credit score is calculated using five major components:

1. Payment History (35%)

This is the largest factor. Paying all bills on time—even small ones—has the biggest impact. A single late payment can drop your score by 60–110 points depending on your profile.

2. Credit Utilization (30%)

This is the percentage of credit you’re using. Goal: Keep utilization below 30%, and ideally under 10% for the fastest score gains.

3. Length of Credit History (15%)

The longer your accounts stay open, the better. This is why closing old accounts can hurt your score.

4. Credit Mix (10%)

Lenders like to see a combination of revolving credit (credit cards) and installment loans (auto loans, student loans, etc.).

5. New Credit (10%)

Too many hard inquiries in a short period can temporarily lower your score.

Typical Credit‑Building Timelines Based on Your Situation

If You Have No Credit History

3–6 months to generate a score

6–12 months to reach 620+

12–24 months to reach 680–720

If You Have Fair Credit (580–620)

3–6 months to reach 620–640

6–12 months to reach 660–680

If You Have Good Credit (660–700)

3–12 months to reach 700–740

12–24 months to reach 740–760+

If You Are Rebuilding After Major Derogatory Events

Late payments: 3–12 months for recovery

Collections: 6–24 months

Bankruptcy: 18–48 months

Foreclosure: 24–60 months

Why Credit Matters So Much in Florida’s Mortgage Market

Florida’s mortgage rates are highly sensitive to credit scores. A borrower with a 760 score may receive an interest rate 0.50%–1.00% lower than someone with a 620 score.

On a $400,000 home (Florida’s median price in many counties), that difference can equal:

$150–$300 per month

$54,000–$108,000 over 30 years

This is why building credit before applying is one of the most financially impactful steps you can take.

How to Build Good Credit Faster: Proven Strategies

1. Pay Every Bill on Time

Since payment history is 35% of your score, this is the #1 factor.

2. Lower Your Credit Utilization

If your credit limit is $5,000, try to keep your balance under:

$1,500 (30%)

$500 (10%) for optimal results

3. Become an Authorized User

If a family member has strong credit, this can boost your score in 30–45 days.

4. Use a Secured Credit Card

Perfect for first‑time credit builders.

5. Keep Old Accounts Open

This helps lengthen your credit history.

6. Avoid Applying for Too Much Credit

Each hard inquiry can drop your score by 5–10 points.

7. Dispute Errors on Your Credit Report

The FTC reports that 1 in 5 Americans has an error on their credit report. Fixing these can lead to immediate score increases.

Florida‑Specific Tips for Mortgage‑Ready Credit

1. Prepare for Higher Insurance Costs

Florida homeowners insurance rates are among the highest in the U.S. Lenders consider your debt‑to‑income ratio (DTI), so improving credit helps offset higher insurance premiums.

2. FHA Loans Are Popular in Florida

Many first‑time buyers use FHA loans due to flexible credit requirements (580+). However, a 620+ score often results in better terms and lower mortgage insurance.

3. Jumbo Loans Require Strong Credit

Florida has many high‑value coastal markets. Jumbo loans typically require:

680–700 minimum score

720+ for best rates

Conclusion: How Long Does It Really Take?

Most Florida homebuyers can build or rebuild good credit for a mortgage in 6 to 24 months, with some improvements appearing in 30–45 days. Whether you’re starting from scratch or recovering from past credit challenges, consistent financial habits and strategic planning can put you on the path to homeownership faster than you might think.

Want personalized assistance? Visit our 'Contact Us' tab and leave your information with one of our experts.

About Us

A group of like-minded seasoned veterans came together to create a company with an employee-focused culture. A culture that values its members both personally and professionally and a company built on the idea that the customer comes first!

We do not share data with third parties for marketing/promotional purposes.

By submitting your phone number to Level Mortgage, you are authorizing a representative of our company to send you text messages and notifications. Message frequency may vary. Message/data rates apply. Reply STOP to unsubscribe to a message sent from us, and HELP to receive help.

Will Home Prices Drop in Florida? 2026 Real Estate Market Trends Explained

Florida’s real estate market has always been dynamic, shaped by migration trends, weather risks, and national economic conditions. As we move into 2026, many buyers and sellers are asking the same question: Will home prices drop? To answer this, let’s break down the latest data, regional variations, and the broader economic forces at play.

– Longer Time on Market: Homes now average 83 days on market, up from 70 days last year, signaling slower demand.

Factors Supporting Price Stability

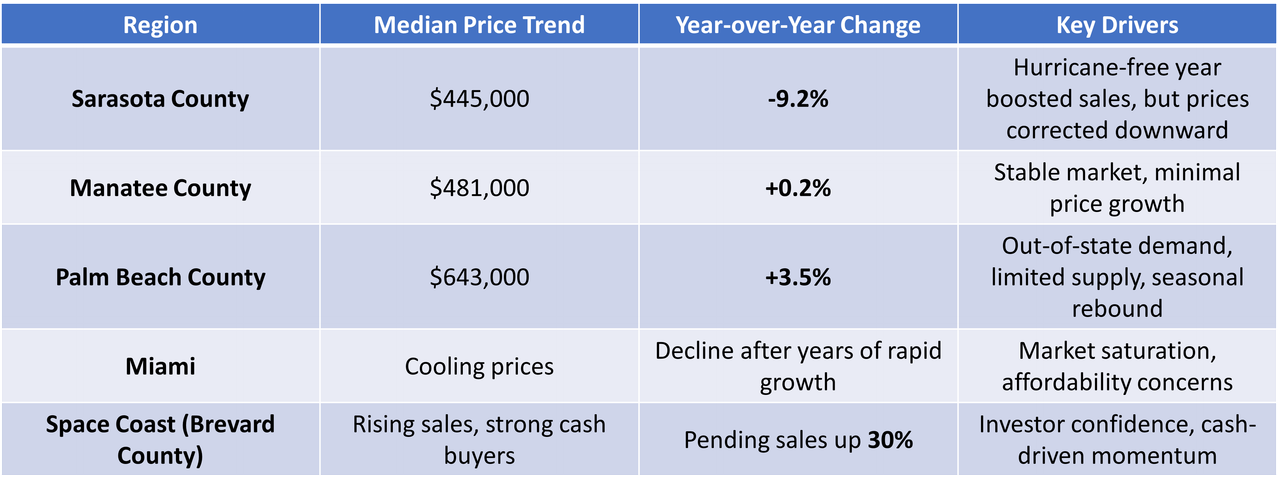

Strong Migration: Florida continues to attract new residents, retirees, and investors, sustaining demand.

Cash Buyers:In areas like the Space Coast, cash purchases surged, insulating the market from mortgage rate fluctuations.

Mortgage Rate Relief: Slight declines in rates (from 6.64% to ~6%) could re-energize buyers in 2026.

Regional Resilience: Counties like Palm Beach and Manatee show steady or rising prices, proving that not all markets are weakening.

2026 Outlook: A “Two-Speed Market”

Experts describe the U.S. housing market as entering a “two-speed” phase:

– Growth Regions: Areas with strong migration (Palm Beach, Space Coast) will likely see modest price increases.

– Correction Regions: Overheated markets (Miami, Sarasota) may continue to decline or flatten.

Florida’s market is unlikely to “crash.” Instead, expect regional divergence: some counties will cool, while others remain competitive.

Key Takeaways for Buyers and Sellers

Experts describe the U.S. housing market as entering a “two-speed” phase:

– Growth Regions: Areas with strong migration (Palm Beach, Space Coast) will likely see modest price increases.

– Correction Regions: Overheated markets (Miami, Sarasota) may continue to decline or flatten.

Florida’s market is unlikely to “crash.” Instead, expect regional divergence: some counties will cool, while others remain competitive.

Conclusion

So, will home prices drop? The answer is nuanced. Yes, in some regions—Sarasota and Miami are already seeing declines. No, in others—Palm Beach and the Space Coast continue to rise. Florida’s housing market in 2026 will be defined by regional divergence, inventory growth, and affordability pressures.

For buyers, this means opportunity. For sellers, it means adjusting expectations. And for the market overall, it means a shift toward balance after years of volatility.

Want personalized assistance? Visit our 'Contact Us' tab and leave your information with one of our experts.

About Us

A group of like-minded seasoned veterans came together to create a company with an employee-focused culture. A culture that values its members both personally and professionally and a company built on the idea that the customer comes first!

We do not share data with third parties for marketing/promotional purposes.

By submitting your phone number to Level Mortgage, you are authorizing a representative of our company to send you text messages and notifications. Message frequency may vary. Message/data rates apply. Reply STOP to unsubscribe to a message sent from us, and HELP to receive help.

5 Expert Tips to Close Your Mortgage Loan Faster (Plus Bonus Strategies)

Want to close your mortgage loan faster? These 5 expert-backed tips—plus bonus strategies—can help you speed up the process, save money, and secure your dream home sooner

Closing a mortgage loan can feel like navigating a maze—paperwork, approvals, inspections, and deadlines. But with the right strategies, you can streamline the process and avoid costly delays. Whether you’re a first-time buyer or refinancing, here are five proven tips to help you close your mortgage loan faster, along with bonus strategies to give you an edge. This guide is brought to you in partnership with Level Mortgage, a trusted name in the mortgage lending space.

Get Pre-Approved, Not Just Pre-Qualified

Pre-approval is a game-changer. Unlike pre-qualification, which is based on self-reported financials, pre-approval involves a lender verifying your income, assets, credit score, and debt-to-income ratio. This gives you a realistic budget and shows sellers you’re serious.

– Level Mortgage’s online portal allows real-time communication and uploads, keeping the process moving.

Schedule Your Appraisal and Inspection ASAP

Appraisals and inspections are often bottlenecks. Book them early to avoid delays:

– Appraisals can take 7–10 business days depending on your market.

– If issues arise during inspection, you’ll need time to negotiate repairs or credits.

Bonus tip: Ask your lender if they offer appraisal waivers for certain loan types—this can save time and money.

Bonus Strategies to Accelerate Closing

Use a Mortgage Broker Like Level Mortgage

Mortgage brokers work with multiple lenders and can match you with one that offers faster underwriting and flexible terms. Level Mortgage specializes in quick closings and personalized service.

Consider Loan Recasting or Refinancing

If you’re refinancing, look into loan recasting—making a lump-sum payment to reduce monthly payments without changing your interest rate or term. It’s faster and less paperwork-intensive than full refinancing.

Opt for a Biweekly Payment Plan

While this doesn’t speed up closing, it helps pay off your mortgage faster post-closing. Making biweekly payments instead of monthly can shave 4–6 years off a 30-year mortgage.

The Bottom Line

Closing a mortgage loan faster is all about preparation, responsiveness, and working with the right professionals. By following these five tips and bonus strategies, you can reduce stress, save money, and move into your new home with confidence.

Want personalized assistance? Visit our 'Contact Us' tab and leave your information with one of our experts.

About Us

A group of like-minded seasoned veterans came together to create a company with an employee-focused culture. A culture that values its members both personally and professionally and a company built on the idea that the customer comes first!

We do not share data with third parties for marketing/promotional purposes.

By submitting your phone number to Level Mortgage, you are authorizing a representative of our company to send you text messages and notifications. Message frequency may vary. Message/data rates apply. Reply STOP to unsubscribe to a message sent from us, and HELP to receive help.

– Many county-level programs offer $7,500 to $15,000 depending on income and location.

These funds can cover:

– FHA’s 3.5% minimum down payment

– Closing costs (title, inspection, appraisal)

– Prepaid taxes and insurance.

Top Programs in Florida

Here are some of the most impactful DPA programs available statewide:

1. Florida Hometown Heroes Program

Offers up to $35,000 for eligible frontline workers (teachers, police, nurses, etc.)

Forgivable loan if you stay in the home for a set period

Must be a first-time buyer or not have owned a home in the past 3 years

2. Florida Assist

Provides $10,000 as a deferred second mortgage

No interest, no monthly payments

Must be used with a Florida Housing first mortgage

3. SHIP (State Housing Initiatives Partnership)

County-administered funds for low-income buyers

Amounts vary by location, often $10,000–$20,000

Can be combined with other programs

4. Local Programs

Miami-Dade, Orange, Hillsborough, and Pinellas counties offer their own grants and loans

Some cities like Tampa and Orlando offer zero-down options for qualified buyers

Who Qualifies?

Eligibility varies, but common requirements include:

– Income limits (typically under 80–120% of area median income)

– Credit score minimums (often 620+)

– Completion of a homebuyer education course

– Primary residence requirement (no investment properties)

You don’t always need to be a first-time buyer. Many programs allow repeat buyers who haven’t owned a home in the past three years, or who are purchasing in designated “target zones”

Why This Matters in 2025

Florida’s housing market remains competitive, with median home prices hovering around $400,000 in many counties. A 3.5% down payment on that is $14,000—not including closing costs. For many families, that’s a dealbreaker.

But with DPA:

– You could pay $0 upfront.

– You could qualify for forgivable loans that never need repayment.

– You could combine programs for maximum benefit.

In fact, tens of thousands of Floridians will receive DPA this year alone.

Persuasive Takeaway: Why You Should Act Now

If you’re renting, you’re already paying someone’s mortgage—just not your own. Down Payment Assistance flips the script. It’s not just financial aid; it’s a wealth-building opportunity.

– Homeownership builds equity: The average Florida homeowner gained over $30,000 in equity in the past two years.

– Rent keeps rising: Florida rents increased by 6.5% in 2024, and are projected to climb again in 2025.

=DPA is time-sensitive: Many programs are funded annually and can run out mid-year.

Next Steps

– Check your eligibility: Use ZIP-code-based tools to find programs near you.

– Take a homebuyer education course: Often required and available online.

– Get pre-approved: Work with a lender familiar with Florida DPA programs.

– Apply early: Funds are limited and awarded on a first-come, first-served basis.

Final Thoughts

Down Payment Assistance isn’t a handout—it’s a hand-up. In 2025, Florida is leading the way in making homeownership accessible. Whether you’re a teacher in Tampa, a nurse in Naples, or a veteran in Jacksonville, there’s a program designed for you.

Don’t let the myth of a massive down payment stop you. With the right guidance and the right program, your dream home is closer than you think.

Want personalized assistance? Visit our 'Contact Us' tab and leave your information with one of our experts.

About Us

A group of like-minded seasoned veterans came together to create a company with an employee-focused culture. A culture that values its members both personally and professionally and a company built on the idea that the customer comes first!

We do not share data with third parties for marketing/promotional purposes.

By submitting your phone number to Level Mortgage, you are authorizing a representative of our company to send you text messages and notifications. Message frequency may vary. Message/data rates apply. Reply STOP to unsubscribe to a message sent from us, and HELP to receive help.

-(10).jpg)