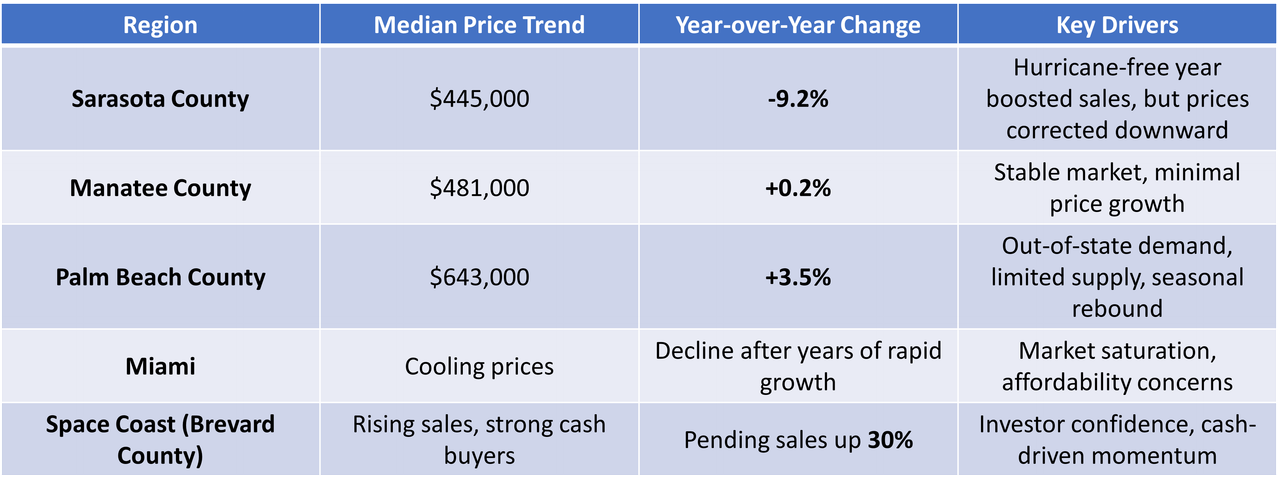

Experts describe the U.S. housing market as entering a “two-speed” phase:

– Growth Regions: Areas with strong migration (Palm Beach, Space Coast) will likely see modest price increases.

– Correction Regions: Overheated markets (Miami, Sarasota) may continue to decline or flatten.