2026 Mortgage Timeline: How Long Does It Take to Close?

Credit Score to Buy a House in 2026

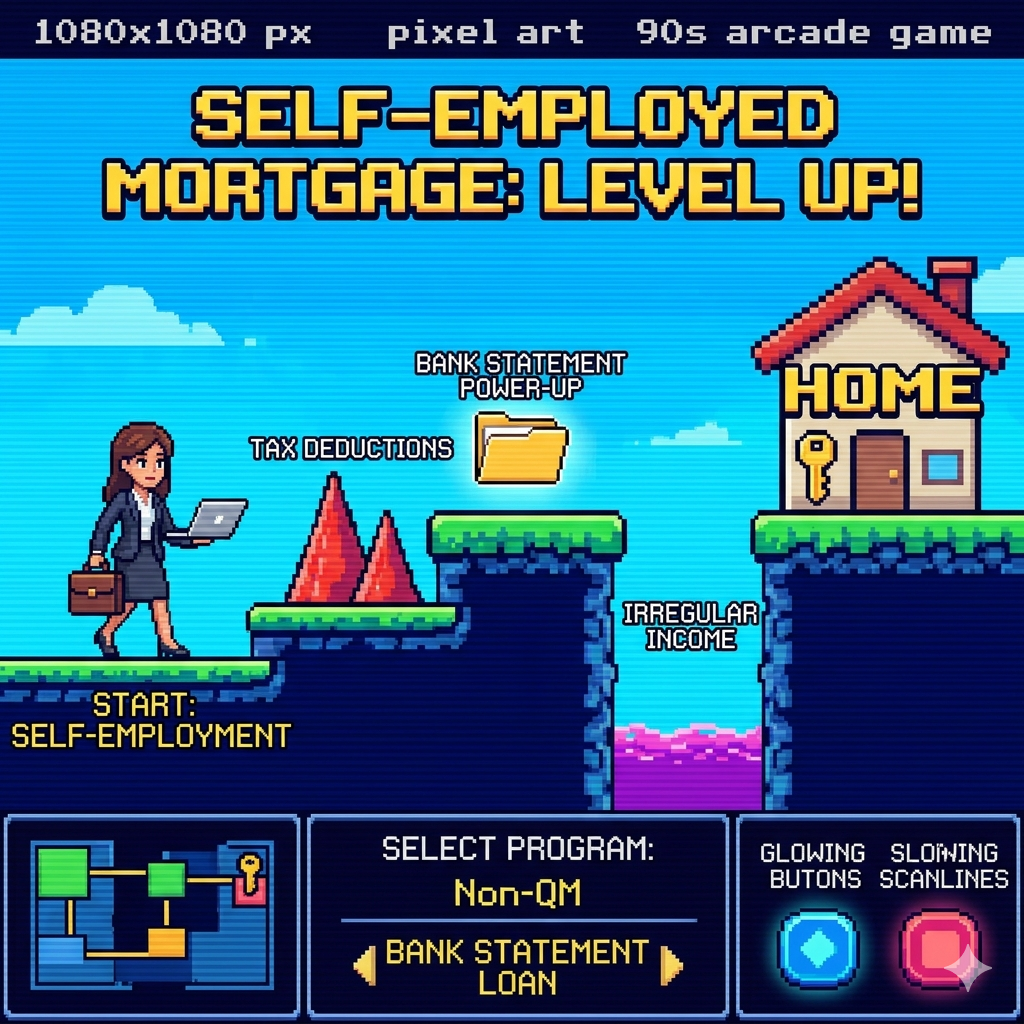

Mortgage Loans for Self-Employed Borrowers | Level Mortgage

How to Finance a New Construction Condo

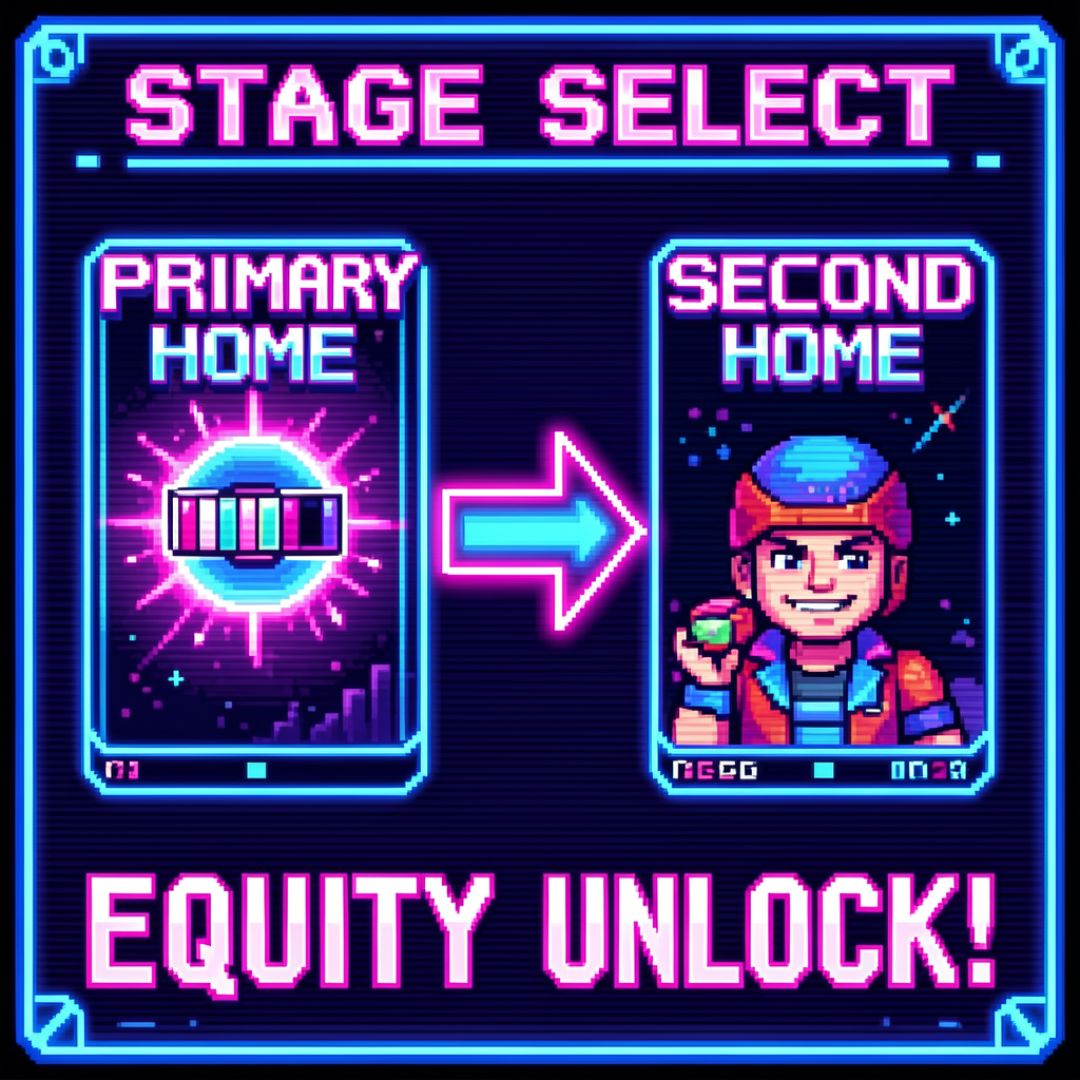

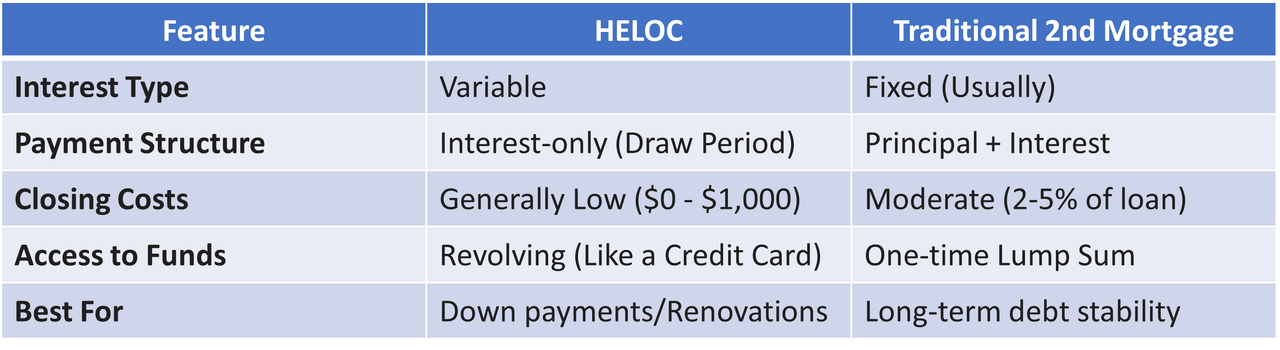

Using a HELOC to Buy a Second Home

-(10).jpg)

The Do’s and Don’ts of Applying for a Mortgage

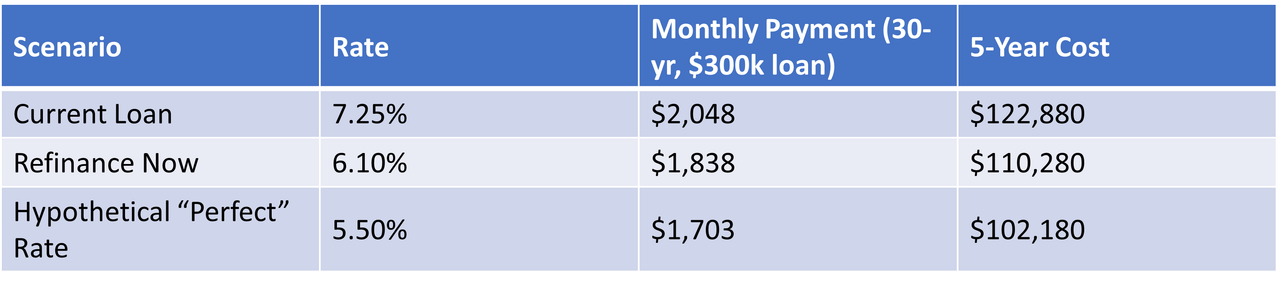

Why Waiting to Refinance Costs More

What Happens After You’re Pre-Approved for a Mortgage

How to Prepare for Your First Mortgage Consultation