Pay Off Your Mortgage Early or Invest? How to Make the Right Financial Move

One of the most common debates among homeowners is whether to funnel extra funds into paying off their mortgage or to deploy that capital into the investment markets. Both paths offer distinct benefits. Paying down debt provides a sense of security and guaranteed returns in the form of interest savings. Investing, on the other hand, offers the potential for higher long-term wealth growth through the power of compounding.

At Level Mortgage, we believe there is no universal right answer. The decision depends entirely on your financial goals, your risk tolerance, your time horizon, and your current mortgage terms. This guide will help you weigh the trade-offs so you can make an informed decision for your unique situation.

The Real Question: Debt Freedom or Wealth Growth?

Choosing between debt repayment and investing is a balancing act. Paying off your mortgage faster essentially “earns” you a return equal to your mortgage interest rate. It is a guaranteed, tax-free return on your money. However, by putting all your extra cash into your home, you may be missing out on higher historical returns in the stock market or other real estate opportunities.

To decide, you must look at your financial life as a whole. Are you prioritizing immediate peace of mind, or are you focused on maximizing your net worth over the next twenty years? Your mortgage rate, your age, and your proximity to retirement are all critical data points in this calculation.

The Benefits of Paying Off Your Mortgage Early

Guaranteed Interest Savings

Every dollar you pay toward your principal reduces the balance upon which your interest is calculated. This creates a compounding effect of interest savings that can save you thousands of dollars over the remaining life of your loan. If you have a high-interest mortgage, this “return” on your money is substantial.

Financial Security and Peace of Mind

For many, the psychological weight of a mortgage is a primary source of stress. Eliminating that monthly obligation provides unparalleled peace of mind. Once your mortgage is paid off, your monthly cash flow increases significantly, providing a buffer against economic downturns or changes in employment.

Building Home Equity Faster

Paying down your principal builds your home equity at an accelerated rate. This increases your net worth and gives you more options for future borrowing, such as using Home Equity Loans to fund major life goals or renovations.

The Benefits of Investing Instead of Paying Off Your Mortgage

Potential Higher Returns

Historical market data often shows that diversified investment portfolios provide returns that exceed current mortgage interest rates. When you pay off a 6% mortgage, your return is exactly 6%. When you invest in a diversified strategy, your long-term potential may be higher, though it comes with more volatility.

The Power of Compound Growth

Investing early allows your money to work for you over decades. Even small monthly contributions can grow into significant wealth because of the time advantage. Investment Market Performance Data highlights how long-term market participation can outperform simple debt repayment, especially for younger homeowners.

Maintaining Liquidity

Money paid into a mortgage is often “trapped” in the home until you sell or refinance. Money in a brokerage account or investment fund remains liquid. In an emergency, it is much easier to access investment funds than it is to pull equity out of your home.

What 2026 Mortgage Rates Mean for This Decision

The 2026 mortgage rate environment is a major factor in your decision. According to recent financial data, mortgage rates have settled into a range that makes the choice more complex than it was during the era of sub-3% rates.

If your current mortgage rate is low, the “cost” of keeping that debt is minimal, and investing those extra funds often makes mathematical sense. If your rate is higher, the “guaranteed return” of paying down your principal becomes much more attractive. Mortgage Rate Data confirms that current rates remain elevated compared to the early 2020s, which is prompting many homeowners to prioritize debt reduction.

Mortgage Interest Rate vs Investment Return: How to Compare

When comparing your mortgage rate to potential investment returns, consider the following:

The “After-Tax” Return: Mortgage interest can sometimes be tax-deductible, which lowers the effective cost of the debt. Conversely, investment gains may be subject to capital gains taxes.

Risk and Volatility: Paying off your mortgage carries zero risk. Investing carries the risk of market loss.

Investment Timeline: The longer your timeline, the more likely you are to ride out market volatility to achieve higher average returns.

Situations Where Paying Off Your Mortgage May Make More Sense

Near Retirement: Many retirees prefer to enter their post-work years without a mortgage payment to minimize monthly expenses.

Low Risk Preference: If you lose sleep over debt, the emotional benefit of being “debt-free” is worth more than any potential market gain.

High Mortgage Interest Rate: If your rate is significantly higher than 6%, paying down the balance provides a robust and risk-free return.

Situations Where Investing May Be the Better Choice

Younger Homeowners: With a multi-decade time horizon, you have the luxury of time to recover from market cycles and benefit from compound growth.

Strong Emergency Savings: If you already have a fully funded emergency reserve, you can afford to take on the market risk associated with investing.

Access to Employer Benefits: If your employer offers a 401(k) match, that is an immediate 100% return on your money. You should always maximize this before paying extra on your mortgage.

A Balanced Strategy: Can You Do Both?

Financial planning is rarely an “either/or” situation. Many homeowners find success by adopting a balanced approach. You can allocate 50% of your extra cash to principal reduction and 50% to a diversified investment account. This allows you to build home equity while simultaneously growing your liquid wealth. This keeps your financial life diversified and flexible.

How Level Mortgage Helps You Make Smarter Mortgage Decisions

At Level Mortgage, we don’t just see a loan; we see a component of your long-term wealth strategy. We help you evaluate your current mortgage terms, run projections on potential Refinance Options, and compare how different payment strategies affect your long-term net worth.

If you are a first-time buyer exploring your options, our First-Time Home Buyer Guide offers a clear roadmap. If you are a seasoned homeowner looking to optimize your debt, we can walk you through the math and help you determine whether your mortgage strategy is aligned with your future goals.

Want personalized assistance? Visit our 'Contact Us' tab and leave your information with one of our experts.

About Us

A group of like-minded seasoned veterans came together to create a company with an employee-focused culture. A culture that values its members both personally and professionally and a company built on the idea that the customer comes first!

We do not share data with third parties for marketing/promotional purposes.

By submitting your phone number to Level Mortgage, you are authorizing a representative of our company to send you text messages and notifications. Message frequency may vary. Message/data rates apply. Reply STOP to unsubscribe to a message sent from us, and HELP to receive help.

Adjustable-Rate Loans Explained: How They Work & When to Get One

Navigating the mortgage landscape in 2026 requires more than just checking the daily interest rates. It involves understanding the tools available to maximize your purchasing power and align your financing with your lifestyle goals. One of the most misunderstood yet potentially powerful tools in a borrower’s arsenal is the Adjustable-Rate Mortgage (ARM). While fixed-rate loans are the industry standard, ARMs offer unique features that may serve specific financial strategies. This guide will help you understand how these loans function and how to determine if one is right for your unique situation.

What Is an Adjustable-Rate Mortgage (ARM)?

An Adjustable-Rate Mortgage is a home loan with an interest rate that can fluctuate over the life of the loan. Unlike a fixed-rate mortgage, where your interest rate and principal and interest payments remain constant for the entire term, an ARM features an initial period of stability followed by a period where the rate adjusts based on market conditions.

Lenders offer ARMs because they provide flexibility for borrowers who do not plan to stay in their homes for 30 years. The rate on an ARM is typically tied to an index, which is a benchmark interest rate that reflects general market conditions. When you add a margin, which is a set percentage determined by the lender, you arrive at the fully indexed rate that determines your payment during the adjustment period.

How Adjustable-Rate Mortgages Work

Understanding an ARM requires looking beyond the initial rate. These loans are built on a specific structure that dictates when and how your payment changes.

The Initial Fixed-Rate Period

Every ARM has an initial period where the interest rate is fixed. This is often represented by two numbers, such as a 5/1 ARM or a 7/1 ARM. The first number represents the years the rate remains fixed. The second number indicates how often the rate can adjust after that period ends. For example, in a 5/1 ARM, your rate is locked for five years. After that, the rate can adjust once every year.

The Adjustment Period

Once the initial fixed period expires, the loan enters the adjustment period. During this time, the lender recalculates your interest rate based on current market indexes. If market rates have risen, your payment may increase. Conversely, if rates have fallen, your payment could decrease. This period continues for the remainder of the loan term, which is typically 30 years.

Rate Caps and Borrower Protections

To protect borrowers from wild fluctuations, ARMs include rate caps.

Initial Adjustment Cap: Limits how much the rate can increase the first time it adjusts.

Periodic Cap: Limits how much the rate can increase from one adjustment period to the next.

Lifetime Cap: Sets a maximum limit on how high the interest rate can rise over the entire life of the loan.

These caps are vital safeguards that prevent your monthly payment from becoming unexpectedly unmanageable.

Why Some Buyers Choose ARMs in 2026

In 2026, the housing market presents unique challenges regarding affordability. Mortgage Rate Trends Report indicates that while rates have stabilized, they remain at a level that pressures the monthly budgets of many homebuyers. Consequently, borrowers are looking for financing options that provide a lower entry point.

Many buyers are exploring ARMs because the initial interest rate is often lower than the rate offered on a traditional fixed-rate loan. This can result in lower monthly payments, which helps borrowers qualify for a higher loan amount. As noted in Housing Affordability Report, strategic financing is becoming a key component for homebuyers looking to enter competitive markets without overextending their monthly cash flow.

Potential Benefits of an Adjustable-Rate Mortgage

Lower Initial Interest Rates

The primary draw of an ARM is the initial lower interest rate. For buyers who plan to move within a few years, this can lead to substantial savings.

Lower Monthly Payments

Lower rates translate directly to lower monthly obligations. This extra breathing room in your budget can be used to pay down other high-interest debt or save for future home maintenance.

Increased Buying Power

Because your initial monthly payment is lower, your debt-to-income ratio may look more favorable to a lender. This can allow you to purchase a home that might have been out of reach under a fixed-rate loan.

Savings for Short-Term Homeowners

If you know you will be in the home for less than the duration of the fixed period, an ARM can be a mathematically superior choice. You capture the lower rate during your entire ownership period and sell or refinance before the first adjustment ever occurs.

Risks Homebuyers Should Understand

While ARMs offer advantages, they carry inherent risks that should not be overlooked.

Future Payment Increases

The most significant risk is the uncertainty of future payments. If market rates rise significantly by the time your adjustment period begins, your monthly housing expense could climb.

Interest Rate Volatility

Market conditions can change rapidly. ARM Market Statistics shows that while ARMs are a stable tool, they are still subject to broader economic shifts that can impact interest rates unexpectedly.

Budgeting Challenges

For homeowners who prefer predictable finances, the variable nature of an ARM can cause stress. It requires a more disciplined approach to financial planning compared to a fixed-rate loan.

When an ARM May Make Sense

An ARM is often a strategic choice rather than a risky gamble. It may make sense if:

You plan to relocate: If you are in a career that requires frequent moves, a 5/1 or 7/1 ARM allows you to take advantage of lower rates for the short time you plan to own the home.

You expect income growth: If you are an early-career professional expecting your salary to increase significantly over the next few years, an ARM can help you manage your budget now, with the peace of mind that you will be able to handle potential payment increases later.

You plan to refinance: If you intend to refinance into a fixed-rate mortgage within a few years, an ARM can bridge the gap.

For those who need long-term stability, a Fixed-Rate Mortgage Guide is generally the safer recommendation. Retirees or those on fixed incomes should carefully consider the risks of payment fluctuations before choosing an ARM.

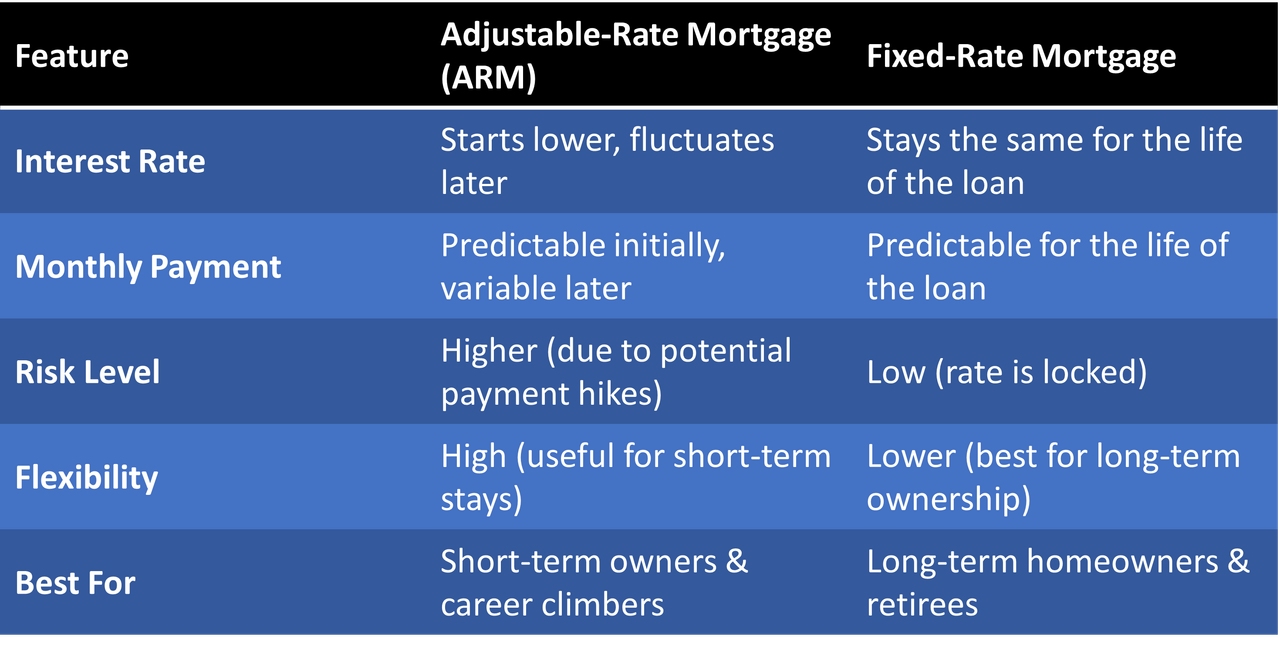

ARM vs Fixed Mortgage: A Side-by-Side Comparison

How Level Mortgage Helps Borrowers Choose the Right Loan

At Level Mortgage, we do not believe in one-size-fits-all financing. We act as your mortgage planners, not just loan processors. We perform comprehensive loan comparison analysis to show you exactly how different products will affect your monthly budget and long-term wealth.

Whether you are applying for Mortgage Pre-Approval or just beginning to navigate the Home Buying Process, our goal is to provide clarity. We want you to feel confident that your mortgage is a strategic asset, not a burden. From evaluating Loan Programs to guiding you through our First-Time Homebuyer Guide, we are here to ensure you understand every aspect of your financial commitment.

Final Thoughts

Adjustable-rate mortgages are sophisticated financial instruments that, when used strategically, can provide significant advantages in affordability and purchasing power. However, they are not suitable for every borrower. The decision to choose an ARM should be based on your unique timeline, your financial flexibility, and your tolerance for market changes. As we look at the Mortgage Industry Forecast for the remainder of 2026, it is clear that borrowers who take the time to evaluate their options will be in the best position to succeed. Connect with Level Mortgage today to begin your loan comparison and find the financing strategy that aligns with your future.

Want personalized assistance? Visit our 'Contact Us' tab and leave your information with one of our experts.

About Us

A group of like-minded seasoned veterans came together to create a company with an employee-focused culture. A culture that values its members both personally and professionally and a company built on the idea that the customer comes first!

We do not share data with third parties for marketing/promotional purposes.

By submitting your phone number to Level Mortgage, you are authorizing a representative of our company to send you text messages and notifications. Message frequency may vary. Message/data rates apply. Reply STOP to unsubscribe to a message sent from us, and HELP to receive help.

What You Need to Know Before Refinancing Your Mortgage

Refinancing your home is one of the most significant financial maneuvers you can perform. As the mortgage landscape shifts in 2026, many homeowners are reevaluating their long-term strategies. Whether you are looking to lower your monthly payments, consolidate high-interest debt, or access your home equity, the decision requires more than just a quick look at interest rates. It demands a comprehensive view of your financial health and long-term goals.

At Level Mortgage, we believe that an informed decision is the only way to proceed. This guide will help you understand the mechanics, costs, and considerations involved in the refinancing process in today’s market.

What Is Mortgage Refinancing?

At its core, refinancing is the process of replacing your existing mortgage with a new loan. When you refinance, you are essentially paying off your current loan and establishing a new one, typically with different terms, interest rates, or loan structures.

In 2026, the process remains relatively straightforward, but the strategic implications are heightened by current economic conditions. Most homeowners refinance to achieve specific financial objectives, such as reducing monthly overhead, shortening their payoff timeline, or extracting cash for other investments. Understanding these mechanics is the first step toward determining if the timing is right for your unique situation. You can learn more about our Mortgage Refinance Programs to see which options align with your goals.

Why Homeowners Refinance

This is the most common motivation. By securing a lower interest rate, you can reduce the amount of interest paid over the life of your loan, which lowers your monthly commitment.In the current 2026 interest rate environment, even a modest reduction in your rate can lead to significant savings over the long term.

Lower Monthly Payments

This is the most common motivation. By securing a lower interest rate, you can reduce the amount of interest paid over the life of your loan, which lowers your monthly commitment.In the current 2026 interest rate environment, even a modest reduction in your rate can lead to significant savings over the long term.

Access Home Equity

If your home has appreciated in value, you may have substantial “tappable” equity. A cash-out refinance allows you to replace your current loan with a larger one and receive the difference in cash. This is frequently used to fund home improvements, pay off high-interest consumer debt, or invest in other assets.Suggests that homeowners currently hold near-record levels of equity, making this a popular route for those looking to leverage their property.

Shorten the Loan Term

Some homeowners choose to refinance from a 30-year mortgage to a 15-year or 20-year term. While this may increase your monthly payment, it significantly reduces the total interest paid over the life of the loan and helps you build equity at an accelerated pace.

Switch Loan Types

You might decide to move from an adjustable-rate mortgage (ARM) to a fixed-rate loan to gain payment stability. Alternatively, some homeowners with FHA or VA loans may seek to refinance into a conventional loan to remove mortgage insurance premiums. If you are exploring this, reviewing [Loan Programs] is a great starting point.

Current Refinance Market Conditions in 2026

The mortgage market in 2026 is defined by a stabilization of rates following the volatility of previous years. Mortgage Rate Trends Report indicates that rates have settled into a more predictable range, though they remain higher than the historic lows seen during the pandemic.

Recent lending statistics indicate that refinance activity is rising as homeowners adjust to this new reality.With many U.S. homeowners sitting on substantial home equity, the ability to tap into those funds has become a major driver of market volume.However, because most homeowners currently have interest rates well below today’s market levels, the “lock-in effect” remains a significant factor in decision-making. You must carefully weigh the cost of moving to a higher rate against the benefits of your specific refinance goals.

How Much Does It Cost to Refinance?

Refinancing is not free. It involves closing costs similar to those you paid when you first purchased your home.

Typical Closing Costs

In 2026, closing costs for a refinance typically range between 2% and 6% of the new loan amount. These fees cover a variety of services, including:

Origination fees: Charged by the lender for processing the new loan.

Appraisal costs: To verify the current market value of your property.

Title fees: To ensure the property title is clean and protected.

Recording fees: Government charges for filing the new mortgage documents.

Calculating Your Break-Even Point

To determine if a refinance is worthwhile, you must calculate your break-even point. This is the amount of time it takes for your monthly savings to cover the total closing costs of the loan.

Example: If your refinance costs $5,000 and saves you $200 per month, your break-even point is 25 months. If you plan to move before that time, the refinance may not be mathematically advantageous. A [INTERNAL LINK: Mortgage Calculator] can help you visualize these numbers.

Qualification Requirements for Refinancing

Lenders look for specific markers of financial stability when evaluating a refinance application.

Credit Score: While standards vary, a higher credit score generally unlocks the best interest rates. Consumer Lending Statisticssuggest that maintaining a score above 700 is typically necessary to access the most competitive pricing.

Debt-to-Income Ratio: Lenders want to see that your total monthly debt payments, including the new mortgage, do not exceed a certain percentage of your gross monthly income.

Home Equity Position: Most lenders require a minimum amount of equity, often represented by a maximum loan-to-value (LTV) ratio.

Income Verification: Expect to provide recent pay stubs, W-2s, or tax returns to prove your ability to repay the loan.

When Refinancing Might Not Make Sense

Refinancing is not a universal solution. It may not be the right choice if:

You plan to move soon: If you sell your home before reaching the break-even point, you will likely lose money on the transaction.

The interest rate spread is too small: If the difference between your current rate and the new rate is negligible, the closing costs may outweigh the savings.

You are resetting your loan term: If you are 20 years into a 30-year mortgage and refinance into a new 30-year loan, you may end up paying significantly more in interest over time, even with a lower payment.

How Level Mortgage Helps Homeowners Make Smarter Refinance Decisions

Refinancing is not a one-size-fits-all product. At Level Mortgage, we act as your strategic partner. We offer personalized mortgage reviews to analyze your current debt structure, your long-term housing plans, and your financial goals. We perform cost-benefit evaluations to ensure that any move you make actually puts you in a stronger position.

Whether you are debating between FHA Loans, VA Loans, or conventional options, we provide the clarity you need to navigate the 2026 market with confidence. We focus on education first, ensuring you understand exactly how your loan strategy impacts your household budget.

Final Thoughts

Refinancing can be an incredibly powerful tool for managing your finances, but it requires careful planning. It is about more than just finding a lower rate; it is about ensuring the structure of your debt aligns with your life goals. As you navigate the 2026 market, remember that professional guidance is an asset. By taking the time to evaluate costs, timing, and long-term impact, you can secure a mortgage strategy that supports your financial well-being for years to come.

Ready to see if refinancing makes sense for your goals?

The best decisions are made with data and expert guidance. Connect with Level Mortgage today for a personalized refinance analysis. We will compare your current mortgage against today’s options and help you determine if a refinance is the strategic move you need.

Want personalized assistance? Visit our 'Contact Us' tab and leave your information with one of our experts.

About Us

A group of like-minded seasoned veterans came together to create a company with an employee-focused culture. A culture that values its members both personally and professionally and a company built on the idea that the customer comes first!

We do not share data with third parties for marketing/promotional purposes.

By submitting your phone number to Level Mortgage, you are authorizing a representative of our company to send you text messages and notifications. Message frequency may vary. Message/data rates apply. Reply STOP to unsubscribe to a message sent from us, and HELP to receive help.

VA Loan Offers: What Home Sellers Really Need to Know

When you list your home for sale, receiving multiple offers is an exciting milestone. Among those purchase contracts, you might find an offer from a buyer utilizing a VA loan. For decades, a cloud of misunderstanding has surrounded this specific financing type, causing some sellers to hesitate.

As a home seller, understanding the true mechanics of VA financing can prevent you from passing up an excellent, secure transaction. Buyers who earn these benefits through military service are often some of the most reliable borrowers in the market. Let’s explore what a VA loan offer actually means for your bottom line.

Why Some Sellers Hesitate When They See a VA Loan Offer

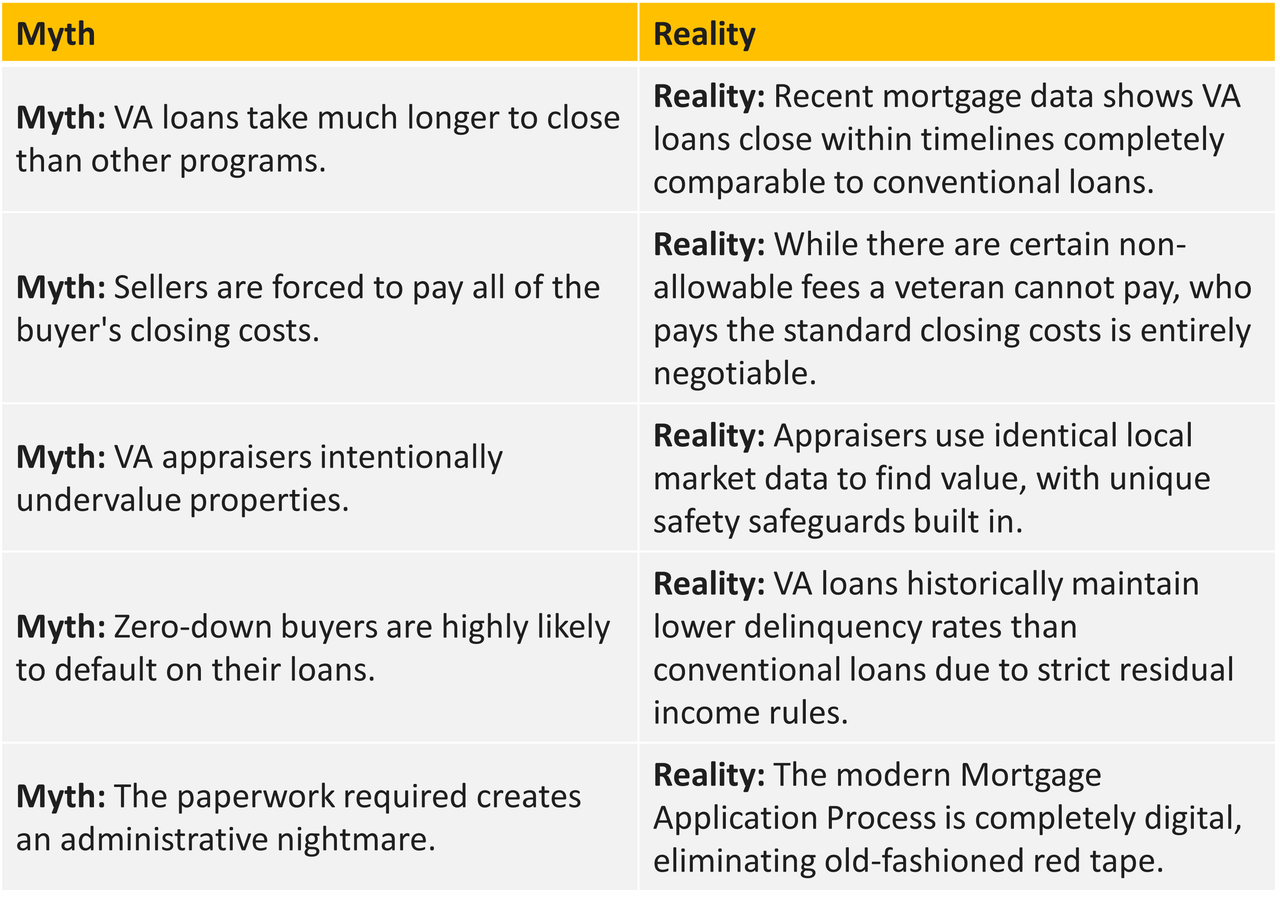

It is common for sellers, and even some real estate agents, to harbor reservations when a VA offer lands on the table. The most frequent misconceptions include the belief that VA loans are much harder to close, that the appraisal process will inevitably compromise the deal, or that VA buyers are less financially secure because they might not make a down payment. Additionally, many people worry that the timeline will drag out indefinitely.

In 2026, these beliefs are remarkably outdated. Modern digital underwriting and updated government guidelines have streamlined the timeline significantly. According to recent mortgage industry data, the closing times for VA loans are neck-and-neck with conventional loans. Furthermore, recent lending data indicates that VA loans actually have a higher overall closing success rate than conventional alternatives, making them an incredibly stable choice for sellers looking for a smooth path to the closing table.

What Makes a VA Loan Different?

To evaluate these offers fairly, it helps to look at how the VA Loan Program operates under the hood.

Backed by the U.S. Department of Veterans Affairs

The defining feature of a VA loan is the government guarantee. The U.S. Department of Veterans Affairs insures a significant portion of the loan amount against default. This structural support drastically reduces the risk for private lenders, allowing them to offer flexible terms to eligible active-duty military members, veterans, and surviving spouses.

Low Down Payment Requirements

One of the most significant perks for military buyers is the ability to secure up to 100% financing. While a conventional seller might view a zero-down offer as a red flag, it is simply a structural advantage given to those who served. A zero-down payment does not reflect a lack of cash reserves or weak purchasing power, it simply means the buyer is leveraging a well-deserved benefit.

Competitive Interest Rates

Because of the federal backing, lenders can offer highly competitive interest rates. Even in the current 2026 lending conditions, where the average mortgage rate environment has settled into a more balanced range, VA loans consistently feature lower interest rates than conventional products. This lower monthly obligation makes the housing payment far more manageable for your buyer, reducing the likelihood of financial stress during escrow.

Are VA Buyers Less Qualified Than Conventional Buyers?

A common myth is that VA buyers are weaker financially. In reality, VA borrowers undergo rigorous qualification standards that often surpass standard conventional guidelines.

Beyond checking credit scores and verifying steady employment income, VA underwriting enforces strict residual income standards. This unique metric calculates how much discretionary cash a family has left over each month after paying all major living expenses and housing costs. Based on trusted housing reports, this safeguard is a major reason why VA loans boast some of the lowest delinquency rates in the entire housing sector.

When you accept a VA offer, you are working with a borrower who has cleared strict federal and institutional hurdles before their Mortgage Pre-Approval ever reaches your hands.

Understanding the VA Appraisal Process

The appraisal process is often the biggest source of anxiety for sellers, but a little clarity can ease those concerns.

What the VA Appraisal Actually Does

Like any appraisal, a VA appraisal determines the fair market value of your property to ensure it matches the agreed-upon purchase price. However, the appraiser also checks the home against a set of Minimum Property Requirements, or MPRs.

Common Property Issues That Can Affect Approval

The MPRs are designed to protect the safety, structural integrity, and sanitation of the property. Common issues that can pop up include:

Major structural deficiencies or foundational issues

Roof concerns, such as a roof nearing the end of its functional life

Exposed or outdated electrical issues

Severe safety hazards, including missing handrails or peeling lead-based paint

Industry research shows that the vast majority of homes pass a VA appraisal without any major issues. If a minor safety item is discovered, it can usually be repaired prior to closing, keeping the transaction perfectly on track.

Benefits of Accepting a VA Loan Offer

When evaluating multiple contracts, keeping an open mind toward VA financing can work to your advantage. Consider these distinct benefits:

Highly Motivated Buyers

Military families often relocate on strict timelines due to Permanent Change of Station orders or transition goals. This makes them highly motivated to cooperate, move quickly, and reach the closing table without unnecessary delays.

Strong Qualification Standards

As noted, strict residual income checks and mandatory document verifications mean these buyers are thoroughly vetted by professionals well before making an offer.

Competitive Purchase Offers

Because VA buyers save money on down payments and monthly mortgage insurance, they often have additional financial flexibility to submit highly competitive purchase offers on homes they love.

What Sellers Should Consider Before Rejecting a VA Offer

In the 2026 real estate landscape, market conditions demand a flexible approach. Inventory levels and buyer demand shift constantly, meaning that judging an offer solely by the loan type can be a costly mistake.

If a VA buyer offers a competitive purchase price, favorable contract terms, and a solid timeline, rejecting them out of hand based on outdated myths could mean leaving money on the table. A well-constructed VA offer can easily compete with, and sometimes outperform, a conventional offer that contains complex contingencies. Look closely at the overall terms of the offer, rather than just the acronym at the top of the page. You can review alternative options in our Loan Programs overview.

VA Loan Myths vs. Reality

How Level Mortgage Helps Buyers and Sellers Navigate VA Transactions

At Level Mortgage, we believe a seamless real estate transaction relies heavily on education, direct communication, and teamwork. We specialize in demystifying the financing process for everyone involved in the sale.

By offering fast pre-approvals and maintaining open lines of communication with listing agents, we ensure sellers feel completely confident when accepting a VA offer. Our experienced strategists coordinate closely with buyers, sellers, and real estate professionals to ensure every property requirement and underwriting milestone is met with speed and accuracy.

Want personalized assistance? Visit our 'Contact Us' tab and leave your information with one of our experts.

About Us

A group of like-minded seasoned veterans came together to create a company with an employee-focused culture. A culture that values its members both personally and professionally and a company built on the idea that the customer comes first!

We do not share data with third parties for marketing/promotional purposes.

By submitting your phone number to Level Mortgage, you are authorizing a representative of our company to send you text messages and notifications. Message frequency may vary. Message/data rates apply. Reply STOP to unsubscribe to a message sent from us, and HELP to receive help.