VA Loan Offers: What Home Sellers Really Need to Know

When you list your home for sale, receiving multiple offers is an exciting milestone. Among those purchase contracts, you might find an offer from a buyer utilizing a VA loan. For decades, a cloud of misunderstanding has surrounded this specific financing type, causing some sellers to hesitate.

As a home seller, understanding the true mechanics of VA financing can prevent you from passing up an excellent, secure transaction. Buyers who earn these benefits through military service are often some of the most reliable borrowers in the market. Let’s explore what a VA loan offer actually means for your bottom line.

Why Some Sellers Hesitate When They See a VA Loan Offer

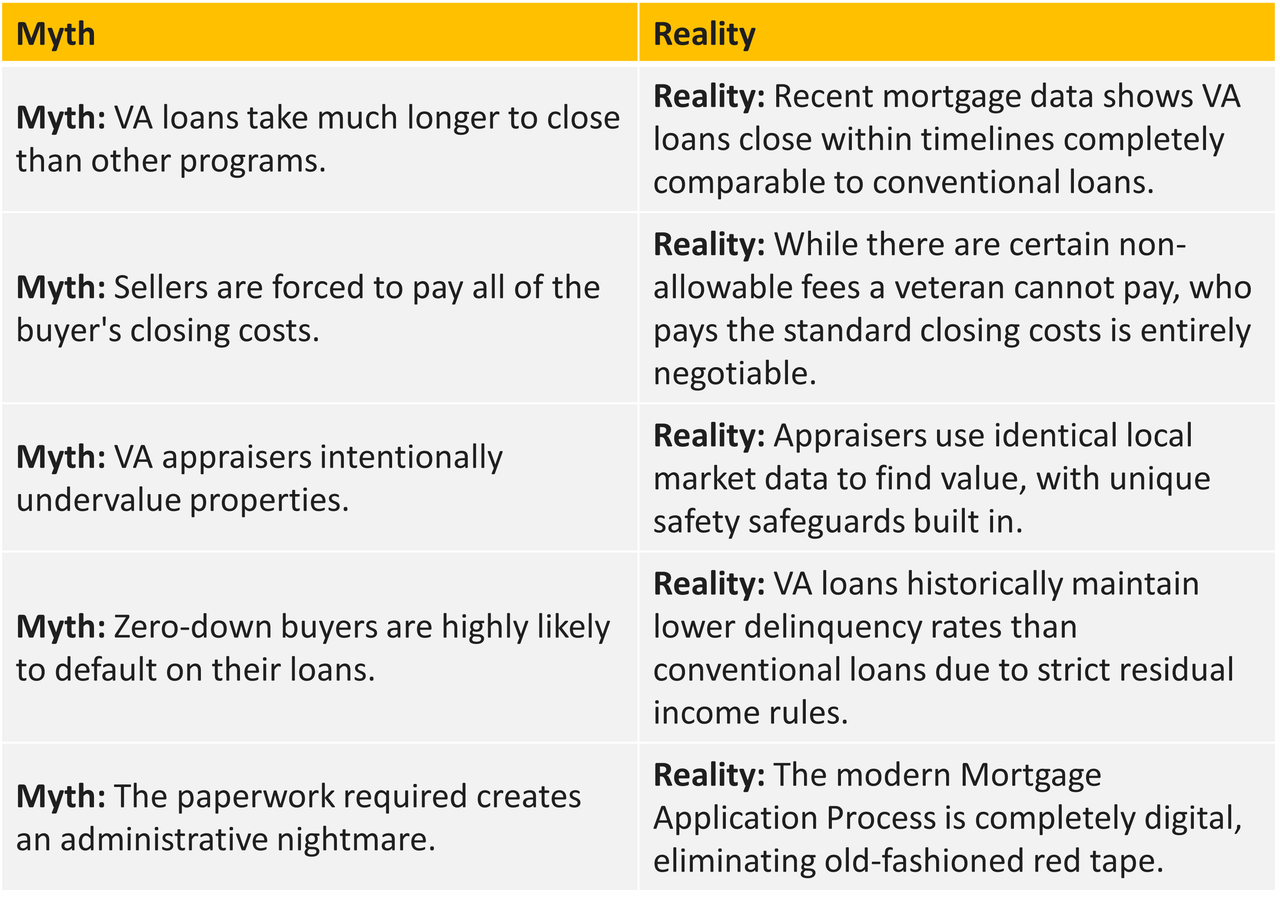

It is common for sellers, and even some real estate agents, to harbor reservations when a VA offer lands on the table. The most frequent misconceptions include the belief that VA loans are much harder to close, that the appraisal process will inevitably compromise the deal, or that VA buyers are less financially secure because they might not make a down payment. Additionally, many people worry that the timeline will drag out indefinitely.

In 2026, these beliefs are remarkably outdated. Modern digital underwriting and updated government guidelines have streamlined the timeline significantly. According to recent mortgage industry data, the closing times for VA loans are neck-and-neck with conventional loans. Furthermore, recent lending data indicates that VA loans actually have a higher overall closing success rate than conventional alternatives, making them an incredibly stable choice for sellers looking for a smooth path to the closing table.

What Makes a VA Loan Different?

To evaluate these offers fairly, it helps to look at how the VA Loan Program operates under the hood.

Backed by the U.S. Department of Veterans Affairs

The defining feature of a VA loan is the government guarantee. The U.S. Department of Veterans Affairs insures a significant portion of the loan amount against default. This structural support drastically reduces the risk for private lenders, allowing them to offer flexible terms to eligible active-duty military members, veterans, and surviving spouses.

Low Down Payment Requirements

One of the most significant perks for military buyers is the ability to secure up to 100% financing. While a conventional seller might view a zero-down offer as a red flag, it is simply a structural advantage given to those who served. A zero-down payment does not reflect a lack of cash reserves or weak purchasing power, it simply means the buyer is leveraging a well-deserved benefit.

Competitive Interest Rates

Because of the federal backing, lenders can offer highly competitive interest rates. Even in the current 2026 lending conditions, where the average mortgage rate environment has settled into a more balanced range, VA loans consistently feature lower interest rates than conventional products. This lower monthly obligation makes the housing payment far more manageable for your buyer, reducing the likelihood of financial stress during escrow.

Are VA Buyers Less Qualified Than Conventional Buyers?

A common myth is that VA buyers are weaker financially. In reality, VA borrowers undergo rigorous qualification standards that often surpass standard conventional guidelines.

Beyond checking credit scores and verifying steady employment income, VA underwriting enforces strict residual income standards. This unique metric calculates how much discretionary cash a family has left over each month after paying all major living expenses and housing costs. Based on trusted housing reports, this safeguard is a major reason why VA loans boast some of the lowest delinquency rates in the entire housing sector.

When you accept a VA offer, you are working with a borrower who has cleared strict federal and institutional hurdles before their Mortgage Pre-Approval ever reaches your hands.

Understanding the VA Appraisal Process

The appraisal process is often the biggest source of anxiety for sellers, but a little clarity can ease those concerns.

What the VA Appraisal Actually Does

Like any appraisal, a VA appraisal determines the fair market value of your property to ensure it matches the agreed-upon purchase price. However, the appraiser also checks the home against a set of Minimum Property Requirements, or MPRs.

Common Property Issues That Can Affect Approval

The MPRs are designed to protect the safety, structural integrity, and sanitation of the property. Common issues that can pop up include:

Major structural deficiencies or foundational issues

Roof concerns, such as a roof nearing the end of its functional life

Exposed or outdated electrical issues

Severe safety hazards, including missing handrails or peeling lead-based paint

Industry research shows that the vast majority of homes pass a VA appraisal without any major issues. If a minor safety item is discovered, it can usually be repaired prior to closing, keeping the transaction perfectly on track.

Benefits of Accepting a VA Loan Offer

When evaluating multiple contracts, keeping an open mind toward VA financing can work to your advantage. Consider these distinct benefits:

Highly Motivated Buyers

Military families often relocate on strict timelines due to Permanent Change of Station orders or transition goals. This makes them highly motivated to cooperate, move quickly, and reach the closing table without unnecessary delays.

Strong Qualification Standards

As noted, strict residual income checks and mandatory document verifications mean these buyers are thoroughly vetted by professionals well before making an offer.

Competitive Purchase Offers

Because VA buyers save money on down payments and monthly mortgage insurance, they often have additional financial flexibility to submit highly competitive purchase offers on homes they love.

What Sellers Should Consider Before Rejecting a VA Offer

In the 2026 real estate landscape, market conditions demand a flexible approach. Inventory levels and buyer demand shift constantly, meaning that judging an offer solely by the loan type can be a costly mistake.

If a VA buyer offers a competitive purchase price, favorable contract terms, and a solid timeline, rejecting them out of hand based on outdated myths could mean leaving money on the table. A well-constructed VA offer can easily compete with, and sometimes outperform, a conventional offer that contains complex contingencies. Look closely at the overall terms of the offer, rather than just the acronym at the top of the page. You can review alternative options in our Loan Programs overview.

VA Loan Myths vs. Reality

How Level Mortgage Helps Buyers and Sellers Navigate VA Transactions

At Level Mortgage, we believe a seamless real estate transaction relies heavily on education, direct communication, and teamwork. We specialize in demystifying the financing process for everyone involved in the sale.

By offering fast pre-approvals and maintaining open lines of communication with listing agents, we ensure sellers feel completely confident when accepting a VA offer. Our experienced strategists coordinate closely with buyers, sellers, and real estate professionals to ensure every property requirement and underwriting milestone is met with speed and accuracy.

Want personalized assistance? Visit our 'Contact Us' tab and leave your information with one of our experts.

About Us

A group of like-minded seasoned veterans came together to create a company with an employee-focused culture. A culture that values its members both personally and professionally and a company built on the idea that the customer comes first!

We do not share data with third parties for marketing/promotional purposes.

By submitting your phone number to Level Mortgage, you are authorizing a representative of our company to send you text messages and notifications. Message frequency may vary. Message/data rates apply. Reply STOP to unsubscribe to a message sent from us, and HELP to receive help.