How the Federal Reserve Impacts Mortgage Rates in 2026

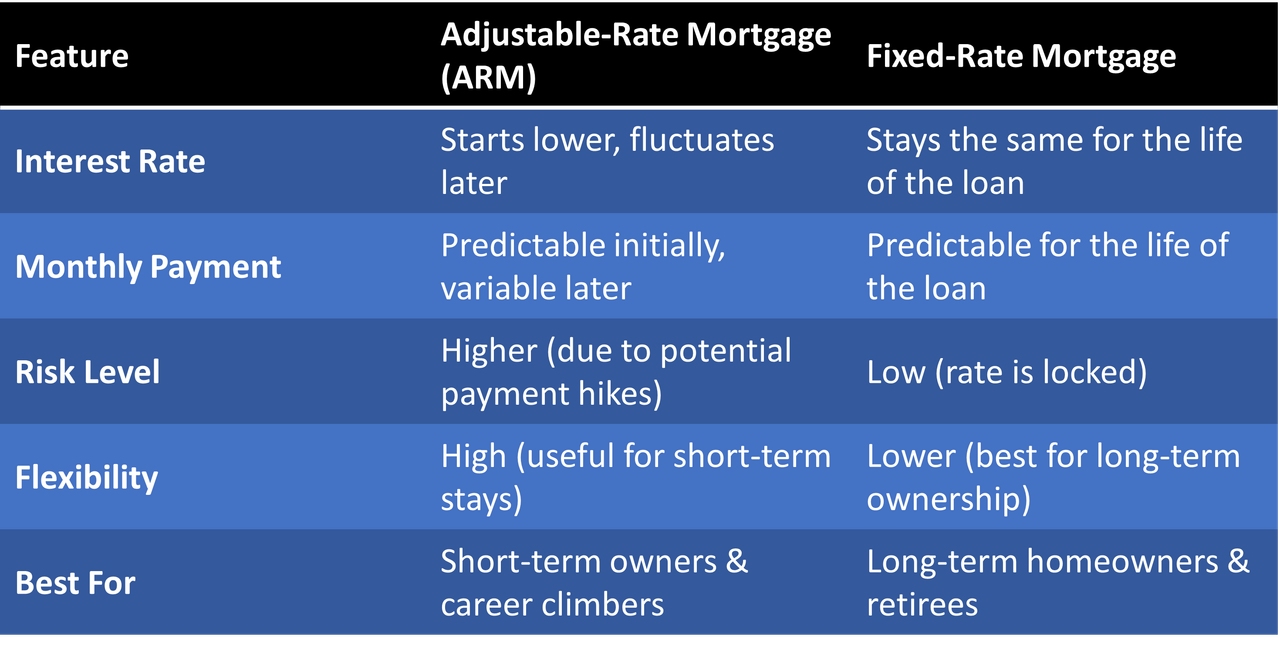

Adjustable-Rate Loans Explained: How They Work & When

What You Need to Know Before Refinancing Your Mortgage in 2026

VA Loan Offers: What Home Sellers Need to Know (2026 Guide)

Multifamily Property Investing: 2026 Guide to Profits and Loans

2026 Mortgage Timeline: How Long Does It Take to Close?

Financing New Construction Condos Before Completion

House Hacking 2026: A Strategy to Buy a Home and Save

Credit Score to Buy a House in 2026